- Social Security (United States)

-

This article is about the retirement/disability program. For the general concept of providing welfare, see Social security. For other uses, see Social Security (disambiguation).

Part of a series of articles on United States

budget and debt topicsMajor dimensions Federal budget · Public debt

Military budget

Expenditures · Taxation

Economy · Financial positionPrograms Medicare · Social Security Contemporary issues Health care reform · Social Security debate

Debt-ceiling crisis

Subprime mortgage crisis

Bush tax cuts · Starve the beast

Bowles-Simpson CommissionTerminology Inflation · Balance of payments  A Social Security card issued in Florida in 1983

A Social Security card issued in Florida in 1983

In the United States, Social Security refers to the federal Old-Age, Survivors, and Disability Insurance (OASDI) program.[1] The original Social Security Act[2] (1935) and the current version of the Act, as amended[3] encompass several social welfare and social insurance programs. The larger and better known programs are:

- Federal Old-Age (Retirement), Survivors, and Disability Insurance

- Unemployment benefits

- Temporary Assistance for Needy Families

- Health Insurance for Aged and Disabled (Medicare)

- Grants to States for Medical Assistance Programs (Medicaid)

- State Children's Health Insurance Program (SCHIP)

- Supplemental Security Income (SSI)

- Patient Protection and Affordable Care Act

Social Security is a social insurance program that is primarily funded through dedicated payroll taxes called Federal Insurance Contributions Act tax (FICA). Tax deposits are formally entrusted to the Federal Old-Age and Survivors Insurance Trust Fund, the Federal Disability Insurance Trust Fund, the Federal Hospital Insurance Trust Fund, or the Federal Supplementary Medical Insurance Trust Fund.[4]

The main part of the program is sometimes abbreviated OASDI (Old Age, Survivors, and Disability Insurance) or RSDI (Retirement, Survivors, and Disability Insurance). When initially signed into law by President Franklin D. Roosevelt in 1935 as part of his New Deal, the term Social Security covered unemployment insurance as well. The term, in everyday speech, is used to refer only to the benefits for retirement, disability, survivorship, and death, which are the four main benefits provided by traditional private-sector pension plans. In 2004 the U.S. Social Security system paid out almost $500 billion in benefits.[5]

By dollars paid, the U.S. Social Security program is the largest government program in the world and the single greatest expenditure in the federal budget, with 20.8% for social security, compared to 20.5% for discretionary defense and 20.1% for Medicare/Medicaid.[6] Social Security is currently the largest social insurance program in the U.S. where in 2003 combined spending for all social insurance programs constituted 37% of government expenditure and 7% of the gross domestic product.[7] Social Security is currently estimated to keep roughly 40 percent of all Americans age 65 or older out of poverty.[8] The Social Security Administration is headquartered in Woodlawn, Maryland, just to the west of Baltimore.

The 2011 annual report by the program's Board of Trustees noted the following: in 2010, 54 million people were receiving Social Security benefits, while 157 million people were paying into the fund; of those receiving benefits, 44 million were receiving retirement benefits and 10 million disability benefits. In 2011, there will be 56 million beneficiaries and 158 million workers paying in. In 2010, total income was $781.1 billion and expenditures were $712.5 billion, which meant a total net increase in assets of $68.6 billion. Assets in 2010 were $2.6 trillion, an amount that is expected to be adequate to cover the next 10 years. In 2023, total income and interest earned on assets are projected to no longer cover expenditures for Social Security, as demographic shifts burden the system. By 2035, the ratio of potential retirees to working age persons will be 37 percent — there will be less than three potential income earners for every retiree in the population. The trust fund would then be exhausted by 2036 without legislative action.[9]

Proposals to privatize Social Security recently became part of the Social Security debate during the Bill Clinton and George W. Bush presidencies.

History

A limited form of the Social Security program began as a measure to implement "social insurance" during the Great Depression of the 1930s, when poverty rates among senior citizens exceeded 50 percent.[10]

Creation: The Social Security Act

President Roosevelt signs the Social Security Act, at approximately 3:30 pm EST on August 14, 1935.[11] Standing with Roosevelt are Rep. Robert Doughton (D-NC); unknown person in shadow; Sen. Robert Wagner (D-NY); Rep. John Dingell (D-MI); unknown man in bowtie; the Secretary of Labor, Frances Perkins; Sen. Pat Harrison (D-MS); and Rep. David Lewis (D-MD).

President Roosevelt signs the Social Security Act, at approximately 3:30 pm EST on August 14, 1935.[11] Standing with Roosevelt are Rep. Robert Doughton (D-NC); unknown person in shadow; Sen. Robert Wagner (D-NY); Rep. John Dingell (D-MI); unknown man in bowtie; the Secretary of Labor, Frances Perkins; Sen. Pat Harrison (D-MS); and Rep. David Lewis (D-MD).The Social Security Act was drafted during Roosevelt's first term by the President's Committee on Economic Security, under Frances Perkins, and passed by Congress as part of the New Deal. The act was an attempt to limit what were seen as dangers in the modern American life, including old age, poverty, unemployment, and the burdens of widows and fatherless children. By signing this act on August 14, 1935, President Roosevelt became the first president to advocate federal assistance for the elderly.[12]

Provisions of the Act

The Act is formally cited as the Social Security Act, ch. 531, 49 Stat. 620, now codified as 42 U.S.C. ch.7. The Act provided benefits to retirees and the unemployed, and a lump-sum benefit at death. Payments to current retirees are financed by a payroll tax on current workers' wages, half directly as a payroll tax and half paid by the employer. The act also gave money to states to provide assistance to aged individuals (Title I), for unemployment insurance (Title III), Aid to Families with Dependent Children (Title IV), Maternal and Child Welfare (Title V), public health services (Title VI), and the blind (Title X).[12]

Initial opposition

Social Security was controversial when originally proposed, with one point of opposition being that it would allegedly cause a loss of jobs. However, proponents argued that there was in fact an advantage: it would encourage older workers to retire, thereby creating opportunities for younger people to find jobs, which would lower the unemployment rate.

Most women and minorities were excluded from the benefits of unemployment insurance and old age pensions. Employment definitions reflected typical white male categories and patterns.[13] Job categories that were not covered by the act included workers in agricultural labor, domestic service, government employees, and many teachers, nurses, hospital employees, librarians, and social workers.[14] The act also denied coverage to individuals who worked intermittently.[15] These jobs were dominated by women and minorities. For example, women made up 90 percent of domestic labor in 1940 and two-thirds of all employed black women were in domestic service.[16] Exclusions exempted nearly half of the working population.[15] Nearly two-thirds of all African Americans in the labor force, 70 to 80 percent in some areas in the South, and just over half of all women employed were not covered by Social Security.[17][18] At the time, the NAACP protested the Social Security Act, describing it as “a sieve with holes just big enough for the majority of Negroes to fall through.”[18]

Some have suggested that this discrimination resulted from the powerful position of Southern Democrats on two of the committees pivotal for the Act’s creation, the Senate Finance Committee and the House Ways and Means Committee.[citation needed] Southern congressmen supported Social Security as a means to bring needed relief to areas in the South that were especially hurt by the Great Depression but wished to avoid legislation which might interfere with the racial status quo in the South. The solution to this dilemma was to pass a bill that both included exclusions and granted authority to the states rather than the national government (such as the states' power in Aid to Dependent Children). Others have argued that exclusions of job categories such as agriculture were frequently left out of new social security systems worldwide because of the administrative difficulties in covering these workers.[18]

Social Security reinforced traditional views of family life.[19] Women generally qualified for benefits only through their husbands or children.[19] Mothers’ pensions (Title IV) based entitlements on the presumption that mothers would be unemployed.[19]

Historical discrimination in the system can also be seen with regard to Aid to Dependent Children. Since this money was allocated to the states to distribute, some localities assessed black families as needing less money than white families. These low grant levels made it impossible for African American mothers to not work: one requirement of the program.[20] Some states also excluded children born out of wedlock, an exclusion which affected African American women more than white women.[21] One study determined that 14.4% of eligible white individuals received funding, but only 1.5 percent of eligible black individuals received these benefits.[18]

Debates on the constitutionality of the Act

In the 1930s, the Supreme Court struck down many pieces of Roosevelt's New Deal legislation, including the Railroad Retirement Act. The Court threw out a centerpiece of the New Deal, the National Industrial Recovery Act, the Agricultural Adjustment Act, and New York State's minimum-wage law. President Roosevelt responded with an attempt to pack the court via the Judiciary Reorganization Bill of 1937. On February 5, 1937, he sent a special message to Congress proposing legislation granting the President new powers to add additional judges to all federal courts whenever there were sitting judges age 70 or older who refused to retire.[22] The practical effect of this proposal was that the President would get to appoint six new Justices to the Supreme Court (and 44 judges to lower federal courts), thus instantly tipping the political balance on the Court dramatically in his favor. The debate on this proposal was heated and widespread, and lasted over six months. Beginning with a set of decisions in March, April, and May, 1937 (including the Social Security Act cases), the Court would sustain a series of New Deal legislation.[23]

Two Supreme Court rulings affirmed the constitutionality of the Social Security Act.

- Steward Machine Company v. Davis, 301 U.S, 548[24] (1937) held, in a 5–4 decision, that, given the exigencies of the Great Depression, "[It] is too late today for the argument to be heard with tolerance that in a crisis so extreme the use of the moneys of the nation to relieve the unemployed and their dependents is a use for any purpose narrower than the promotion of the general welfare". The arguments opposed to the Social Security Act (articulated by justices Butler, McReynolds, and Sutherland in their opinions) were that the social security act went beyond the powers that were granted to the federal government in the Constitution. They argued that, by imposing a tax on employers that could be avoided only by contributing to a state unemployment-compensation fund, the federal government was essentially forcing each state to establish an unemployment-compensation fund that would meet its criteria, and that the federal government had no power to enact such a program.

- Helvering v. Davis, 301 U.S. 619 (1937), decided on the same day as Steward, upheld the program because "The proceeds of both [employee and employer] taxes are to be paid into the Treasury like internal-revenue taxes generally, and are not earmarked in any way". That is, the Social Security Tax was constitutional as a mere exercise of Congress's general taxation powers.

Ida May Fuller, the first recipient

Ida May Fuller, the first recipientImplementation

Payroll taxes were first collected in 1937, also the year in which the first benefits were paid, namely the lump-sum death benefit paid to 53,236 beneficiaries.[citation needed]

The first reported Social Security payment was to Ernest Ackerman, who retired only one day after Social Security began. Five cents were withheld from his pay during that period, and he received a lump-sum payout of seventeen cents from Social Security.[25]

The first monthly payment was issued on January 31, 1940 to Ida May Fuller of Ludlow, Vermont. In 1937, 1938 and 1939 she paid a total of $24.75 into the Social Security System. Her first check was for $22.54. After her second check, Fuller already had received more than she contributed over the three-year period. She lived to be 100 and collected a total of $22,888.92.[26]

Expansion and evolution

Further information: List of Social Security legislation (United States)The provisions of Social Security have been changing since the 1930s, shifting in response to economic worries as well as concerns over changing gender roles and the position of minorities. Officials have responded more to the concerns of women than those of minority groups.[27] Social Security gradually moved toward universal coverage. By 1950, debates moved away from which occupational groups should be included to how to provide more adequate coverage.[28] Changes in Social Security have reflected a balance between promoting equality and efforts to provide adequate protection.[29]

In 1940, benefits paid totaled $35 million. These rose to $961 million in 1950, $11.2 billion in 1960, $31.9 billion in 1970, $120.5 billion in 1980, and $247.8 billion in 1990 (all figures in nominal dollars, not adjusted for inflation). In 2004, $492 billion of benefits were paid to 47.5 million beneficiaries.[30] In 2009, nearly 51 million Americans received $650 billion in Social Security benefits.

1939 Amendments

Economic concerns

One reason for the proposed changes in 1939 was a growing concern over the impact that the reserves created by the 1935 act were having on the economy. The Recession of 1937 was blamed on the government, tied to the abrupt decrease in government spending and the $2 billion that had been collected in Social Security taxes.[31] Benefits became available in 1940 instead of 1942 and changes to the benefit formula increased the amount of benefits available to all recipients in the early years of Social Security.[32] These two policies combined to shrink the size of the reserves. The original Act had conceived of the program as paying benefits out of a large reserve. This Act shifted the conception of Social Security into something of a hybrid system; while reserves would still accumulate, most early beneficiaries would receive benefits on the pay-as-you-go system. Just as importantly, the changes also delayed planned rises in contribution rates. Ironically if these had been left in place they would have come into effect during the wartime boom in wages and would have arguably helped to temper wartime inflation.[33]

Creation of the Social Security Trust Fund

The amendments established a trust fund for any surplus funds. The managing trustee of this fund is the Secretary of the Treasury. The money could be invested in both non-marketable and marketable securities.[34]

The move toward family protection

Calls for reform of Social Security emerged within a few years of the 1935 Act. Even as early as 1936, some believed that women were not getting enough support. Worried that a lack of assistance might push women back into the work force, these individuals wanted Social Security changes that would prevent this. In an effort to protect the family, therefore, some called for reform which tied women's aid more concretely to their dependency on their husbands.[35] Others expressed apprehension about the complicated administrative practices of Social Security.[36] Concerns about the size of the reserve fund of the retirement program, emphasized by a recession in 1937 led to further calls for change.[37]

These amendments, however, avoided the question of the large numbers of workers in excluded categories.[38] Instead, the amendments of 1939 made family protection a part of Social Security. This included increased federal funding for the Aid to Dependent Children and raised the maximum age of children eligible to receive money under the Aid to Dependent Children to 18. The amendment added wives, elderly widows, and dependent survivors of covered male workers to those who could receive old age pensions. These individuals had previously been granted lump sum payments upon only death or coverage through the Aid to Dependent Children program. If a married wage-earning woman’s own benefit was worth less than 50% of her husband’s benefit, she was treated as a wife, not a worker.[39] If a woman who was covered by Social Security died, however, her dependents were ineligible for her benefits.[40] Since support for widows was dependent on the husband being a covered worker, African American widows were severely underrepresented and unaided by these changes.[41]

In order to assure fiscal conservatives who worried about the costs of adding family protection policies, the benefits for single workers were decreased and lump-sum death payments were abolished.[42]

FICA

A poster for the expansion of the Social Security Act

A poster for the expansion of the Social Security ActIn the original 1935 law, the benefit provisions were in Title II of the Act (which is why Social Security is sometimes referred to as the "Title II" program.) The taxing provisions were in a separate title (Title VIII) (for reasons related to the constitutionality of the 1935 Act). As part of the 1939 Amendments, the Title VIII taxing provisions were taken out of the Social Security Act and placed in the Internal Revenue Code and renamed the Federal Insurance Contributions Act (FICA). Social Security payroll taxes thus often referred to as "FICA taxes."

Since FICA taxes do not fund "retirement accounts" analogous to investment accounts such as IRAs, it has been argued that returns on these contributions are not comparable to returns on private investment instruments. But because Social Security contributions are nonetheless arguably analogous to pooled insurance premiums[43] (as they protect workers and covered family members against loss of income from the wage earner's retirement, disability, or death) it may be appropriate to compare the return on the "risk pool of funds" garnered by Social Security with the return on the "risk pool of funds" garnered by a for-profit commercial insurance company. Like any insurance program, Social Security "spreads risk". For example, a worker who becomes disabled at a young age could receive a large return relative to the amount they contributed in FICA before becoming disabled, since disability benefits can continue for life. As in private insurance plans, everyone in the particular insurance pool is insured against the same risks, but not everyone will benefit to the same extent.

The analogy to insurance, however, is limited[44] by the fact that paying FICA taxes creates no legal right to benefits and by the extent to which Social Security is, in fact, funded by FICA taxes. The 2010 "Obama-GOP tax deal", for example, cut FICA taxes with the impact on Social Security's solvency neutralized by a transfer from general revenues. These transfers add to the general budget deficit like general program spending.[45][46][47]

Amendments of the 1950s

After years of debates about the inclusion of domestic labor, household employees working at least two days a week for the same person were added in 1950, along with nonprofit workers and the self-employed. Hotel workers, laundry workers, all agricultural workers, and state and local government employees were added in 1954.[48]

In 1956, the tax rate was raised to 4.0 percent (2.0 percent for the employer, 2.0 percent for the employee) and disability benefits were added. Also in 1956, women were allowed to retire at 62 with benefits reduced by 25 percent. Widows of covered workers were allowed to retire at 62 without the reduction in benefits.[49]

Amendments of the 1960s

Brochure from 1961 with basic advice about Social Security cards (pages 1 and 4)

Brochure from 1961 with basic advice about Social Security cards (pages 1 and 4) Same brochure (pages 2 and 3)

Same brochure (pages 2 and 3)In 1961, retirement at age 62 was extended to men, and the tax rate was increased to 6.0%.

In 1962, the changing role of the female worker was acknowledged when benefits of covered women could be collected by dependent husbands, widowers, and children. These individuals, however, had to be able to prove their dependency.[50]

Medicare and Medicaid were added in 1965 by the Social Security Act of 1965, part of President Lyndon B. Johnson's "Great Society" program.

In 1965, the age at which widows could begin collecting benefits was reduced to 60. Widowers were not included in this change. When divorce, rather than death, became the major cause of marriages ending, divorcées were added to the list of recipients. Divorcées over the age of 65 who had been married for at least 20 years, remained unmarried, and could demonstrate dependency on their ex-husbands received benefits.[51]

The government adopted a unified budget in the Johnson administration in 1968. This change resulted in a single measure of the fiscal status of the government, based on the sum of all government activity.[52] The surplus in Social Security trust funds offsets the total debt, making it appear much smaller than it otherwise would.

Amendments of the 1970s

1972 Amendments

In June 1972, both houses of the United States Congress approved by overwhelming majorities 20% increases in benefits for 27.8 million Americans. The average payment per month rose from $133 to $166. The bill also set up a cost-of-living adjustment (COLA) to take effect in 1975. This adjustment would be made on a yearly basis if the Consumer Price Index (CPI) increased by 3% or more.[53] This addition was an attempt to index benefits to inflation so that benefits would rise automatically. If inflation was 5%, the goal was to automatically increase benefits by 5% so their real value didn't decline. A technical error in the formula caused these adjustments to overcompensate for inflation, a technical mistake which has been called double-indexing. The COLAs actually caused benefits to increase at twice the rate of inflation.

In October 1972, a $5 billion piece of Social Security legislation was enacted which expanded the Social Security program. For example, minimum monthly benefits of individuals employed in low income positions for at least 30 years were raised. Increases were also made to the pensions of 3.8 million widows and dependent widowers.[53]

These amendments also established the Supplemental Security Income (SSI). SSI is not a Social Security benefit, but a welfare program, because the elderly and disabled poor are entitled to SSI regardless of work history. Likewise, SSI is not an entitlement, because there is no right to SSI payments.

The negative financial outlook

Throughout the 1950s and 1960s, during the phase-in period of Social Security, Congress was able to grant generous benefit increases because the system had perpetual short-run surpluses. Congressional amendments to Social Security took place in even numbered years (election years) because the bills were politically popular, but by the late 1970s, this era was over. For the next three decades, projections of Social Security's finances would show large, long-term deficits, and in the early 1980s, the program flirted with immediate insolvency. From this point on, amendments to Social Security would take place in odd numbered years (years that were not election years) because Social Security reform now meant tax increases and benefit reductions. Social Security became known as the "Third Rail of American Politics." Touching it meant political death.

Several effects came together in the years following the 1972 amendments which rapidly changed the outlook on Social Security's long-term financial picture from positive to problematic. By the 1970s, the phase-in period, during which workers were paying taxes but few were collecting benefits, was largely over, and the ratio of elderly population to the working population was increasing. These developments brought questions about the capacity of the long term financial structure based on a pay-as-you-go program.

During the Carter administration, the economy suffered double-digit inflation, coupled with very high interest rates, oil and energy crises, high unemployment and slow economic growth. Productivity growth in the United States had declined to an average annual rate of 1%, compared to 3.2% during the 1960s. There was also a growing federal budget deficit which increased to $66 billion. The 1970s are described as a period of stagflation, meaning economic stagnation coupled with price inflation, as well as higher interest rates. Price inflation (a rise in the general level of prices) creates uncertainty in budgeting and planning and makes labor strikes for pay raises more likely.

These underlying negative trends were exacerbated by a colossal mathematical error made in the 1972 amendments establishing the COLAs. The mathematical error which overcompensated for inflation was particularly detrimental given the double-digit inflation of this period, and the error led to benefit increases that were nowhere near financially sustainable.

The high inflation, double-indexing, and lower than expected wage growth was financial disaster for Social Security.

1977 Amendments

To combat the declining financial outlook, in 1977 Congress passed and Carter signed legislation fixing the double-indexing mistake. This amendment also altered the tax formulas to raise more money,[54] increasing withholding from 2% to 6.15%.[55] With these changes, President Carter remarked, "Now this legislation will guarantee that from 1980 to the year 2030, the Social Security funds will be sound."[56] This turned out not to be the case. The financial picture declined almost immediately and by the early 1980s, the system was again in crisis.

Amendments of the 1980s

After the 1977 amendments, the economic assumptions surrounding Social Security projections continued to be overly optimistic as the program moved toward a crisis. For example, COLAs were attached to increases in the CPI. This meant that they changed with prices, instead of wages. Before the 1970s, wage measurements exceeded changes in price. In the 1970s, however, this reversed and real wages decreased. This meant that FICA revenues could not keep up with the increasing benefits that were being given out. Continued high unemployment levels also lowered the amount of Social Security tax that could be collected. These two developments were decreasing the Social Security Trust Fund reserves.[57] In 1982, projections indicated that the Social Security Trust Fund would run out of money by 1983, and there was talk of the system being unable to pay benefits.[58] The National Commission on Social Security Reform, chaired by Alan Greenspan, was created to address the crisis.

The 1983 Amendments

The National Commission on Social Security Reform (NCSSR), chaired by Alan Greenspan, was empaneled to investigate the long-run solvency of Social Security. The 1983 Amendments to the SSA were based on the NCSSR's Final Report.[59] The NCSSR recommended enacting a six-month delay in the COLA and changing the tax-rate schedules for the years between 1984 and 1990.[60] It also proposed an income tax on the Social Security benefits of higher-income individuals. This meant that benefits in excess of a household income threshold, generally $25,000 for singles and $32,000 for couples (the precise formula computes and compares three different measures) became taxable. These changes were important for generating revenue in the short term.

Also of concern was the long-term prospect for Social Security because of demographic considerations. Of particular concern was the issue of what would happen when people born during the post–World War II baby boom retired. The NCSSR made several recommendations for addressing the issue.[61] Under the 1983 amendments to Social Security, a previously enacted increase in the payroll tax rate was accelerated, additional employees were added to the system, the full-benefit retirement age was slowly increased, and up to one-half of the value of the Social Security benefit was made potentially taxable income.[62][63]

The 1983 Amendments and the Social Security Trust Fund

The 1983 Amendments also included a provision to exclude the Social Security Trust Fund from the unified budget (In political jargon, it was proposed to be taken “off-budget.”[citation needed] Yet today Social Security is treated like all the other trust funds of the Unified Budget.[citation needed] It is a political way of using a cash budget instead of the more appropriate accrual budget (for all the budgets in the U.S. government), and a way of disguising total debt.[64] This provision also provided for the exemption of Social Security and portions of the Medicare trust funds from any general budget cuts beginning in 1993.[52] This change was one way of trying to protect Social Security funds for the future.

As a result of these changes, particularly the tax increases, the Social Security system began to generate a large short-term surplus of funds, intended to cover the added retirement costs of the "baby boomers." Congress invested these surpluses into special series, non-marketable U.S. Treasury securities held by the Social Security Trust Fund. Under the law, the government bonds held by Social Security are backed by the full faith and credit of the U.S. government.

The Supreme Court and the evolution of Social Security

The Supreme Court has established that no one has any legal right to Social Security benefits. The Court decided, in Flemming v. Nestor (1960), that "entitlement to Social Security benefits is not a contractual right". In that case, Ephram Nestor, a Bulgarian immigrant to the United States who made contributions for covered wages for the statutorily required "quarters of coverage" was nonetheless denied benefits after being deported in 1956 for being a member of the Communist party.

The case specifically held:

2. A person covered by the Social Security Act has not such a right in old-age benefit payments as would make every defeasance of "accrued" interests violative of the Due Process Clause of the Fifth Amendment. Pp. 608–611. (a) The noncontractual interest of an employee covered by the Act cannot be soundly analogized to that of the holder of an annuity, whose right to benefits are based on his contractual premium payments. Pp. 608–610. (b) To engraft upon the Social Security System a concept of "accrued property rights" would deprive it of the flexibility and [363 U.S. 603, 604] boldness in adjustment to ever-changing conditions which it demands and which Congress probably had in mind when it expressly reserved the right to alter, amend or repeal any provision of the Act. Pp. 610–611. 3. Section 202 (n) of the Act cannot be condemned as so lacking in rational justification as to offend due process. Pp. 611–612. 4. Termination of appellee's benefits under 202 (n) does not amount to punishing him without a trial, in violation of Art. III, 2, cl. 3, of the Constitution or the Sixth Amendment; nor is 202 (n) a bill of attainder or ex post facto law, since its purpose is not punitive. Pp. 612–621.[65]

The Supreme Court was also responsible for major changes in Social Security. Many of these cases were pivotal in changing the assumptions about differences in wage earning among men and women in the Social Security system.[65]

- Goldberg v. Kelly (1970): The Supreme Court ruled that the due process clause of the Fourteenth Amendment required there to be an evidentiary hearing before a recipient can be deprived of government benefits.[29]

- Weinberger v. Wiesenfeld (1975): A widower claimed that he was entitled to his deceased wife’s benefit, even though he had not been dependent on his wife. The court upheld his claims, stating that automatically granting widows the benefits and denying them to widowers violated equal protection in the Fourteenth Amendment.[66]

Dates of coverage for various workers

- 1935 All workers in commerce and industry (except railroads) under age 65.

- 1939 Age restriction eliminated; seamen, bank employees added; additional domestic workers and food-processing workers removed

- 1946 Railroad and Social Security earnings combined to determine eligibility for and amount of survivor benefits.

- 1950 Regularly employed farm and domestic workers. Nonfarm self-employed (except professional groups). Federal civilian employees not under retirement system. Americans employed outside United States by American employer. Puerto Rico and Virgin Islands. At the option of the State, State and local government employees not under retirement system. Nonprofit organizations could elect coverage for their employees (other than ministers).

- 1951 Railroad workers with less than 10 years of service, for all benefits. (After October 1951, coverage is retroactive to 1937.)

- 1954 Farm self-employed. Professional self-employed except lawyers, dentists, doctors, and other medical groups. Additional regularly employed farm and domestic workers. Homeworkers. State and local government employees (except firemen and policemen) under retirement system if agreed to by referendum. Ministers could elect coverage as self-employed.

- 1956 Members of the uniformed services. Remainder of professional self-employed except doctors. By referendum, firemen and policemen in designated States.

- 1965 Interns. Self-employed doctors. Tips.

- 1967 Ministers (unless exemption is claimed on grounds of conscience or religious principles). Firemen under retirement system in all States.

- 1972 Members of a religious order subject to a vow of poverty.

- 1983 All federal civilian employees hired after 1983; members of Congress, the President and Vice-President and federal judges; all employees of nonprofit organizations. Covered state and local government employees prohibited from opting out of Social Security.

- 1990 Employees of state and local governments not covered under a retirement plan.[67]

Benefits

The largest component of OASDI is the payment of retirement benefits. Throughout a worker's career, the Social Security Administration keeps track of his or her earnings. The amount of the monthly benefit to which the worker is entitled depends upon that earnings record and upon the age at which the retiree chooses to begin receiving benefits. For the entire history of Social Security, benefits have been paid almost entirely by using revenue from payroll taxes. This is why Social Security is referred to as a pay-as-you-go system. Around 2017, payroll tax revenue is projected to be insufficient to cover Social Security benefits[citation needed] and the system will begin to withdraw money from the Social Security Trust Fund. The existence and economic significance of the Social Security Trust Fund is a subject of considerable dispute because its assets are special Treasury bonds; i.e. the money in the trust fund has been lent back to the federal government to pay for other expenses.

Totals By Year

- Year – Beneficiaries – Dollars

- 1937 – 53,236 – $1,278,000

- 1938 – 213,670 – $10,478,000

- 1939 – 174,839 – $13,896,000

- 1940 – 222,488 – $35,000,000

- 1950 – 3,477,243 – $961,000,000

- 1960 – 14,844,589 – $11,245,000,000

- 1970 – 26,228,629 – $31,863,000,000

- 1980 – 35,584,955 – $120,511,000,000

- 1990 – 39,832,125 – $247,796,000,000

- 1995 – 43,387,259 – $332,553,000,000

- 1996 – 43,736,836 – $347,088,000,000

- 1997 – 43,971,086 – $361,970,000,000

- 1998 – 44,245,731 – $374,990,000,000

- 1999 – 44,595,624 – $385,768,000,000

- 2000 – 45,414,794 – $407,644,000,000

- 2001 – 45,877,506 – $431,949,000,000

- 2002 – 46,444,317 – $453,746,000,000

- 2003 – 47,038,486 – $470,778,000,000

- 2004 – 47,687,693 – $493,263,000,000

- 2005 – 48,434,436 – $520,748,000,000

- 2006 – 49,122,624 – $546,238,000,000

- 2007 – 49,864,838 – $584,939,000,000

- 2008 – 50,898,244 – $615,344,000,000

Primary Insurance Amount

A worker's retirement income benefit is based on his Primary Insurance Amount, or PIA. The PIA is the average of the highest 35 years of the worker's covered earnings (before deduction for FICA). Covered earnings in any year are limited by that year's Social Security Wage Base, the maximum earnings that could be subject to the OASDI portion of FICA payroll tax ($106,800 in 2010[68]). If the worker has fewer than 35 years of covered earnings, zeros are used to bring the total number of years of earnings up to 35. Years of covered work more than 2 years before the year the worker turns 62 are indexed upward to reflect the increase in the national wage via the average wage index (AWI) from the time at which the earnings were covered in the past to the value of the AWI two years before the worker turns 62 (which is the most recent year available at the date the worker turns 62). One-twelfth of this 35-year average is the average indexed monthly earnings (AIME). The PIA then is 90 percent of the AIME up to the first (low) bendpoint, and 32 percent of the excess of AIME over the first bendpoint but not in excess of the second (high) bendpoint, plus 15 percent of the AIME in excess of the second bendpoint. Bendpoints designate the point at which the rates of return on a beneficiary's AIME change.[69][70] In 2008, the bendpoints for calculating the PIA are a change from 90% to 32% at $711 and a change to 15% at $4,288.[70][71] This PIA is then adjusted by automatic cost-of-living adjustments annually starting with the year the worker turns 62. Similar computations based on career average earnings determine disability and survivor benefits. These alternate computations average less years of earnings when the worker dies or is disabled before age 62 and use different base years for the inflation adjustments.

Normal retirement age

Main article: Retirement Insurance BenefitsThe earliest age at which (reduced) benefits are payable is 62. Full retirement benefits depend on a retiree's year of birth.[72] Those born before 1938 have a normal retirement age of 65. Normal retirement age increases by two months for each ensuing year of birth until the 1943 year of birth, when it stays at age 66 years until the year of birth 1955. Thereafter the normal retirement age increases again by two months for each year ending in the 1960 year of birth, when normal retirement age stops at age 67 for all born thereafter. Since the retirement age increases each year it is important to look at how the rest of the world is vastly approaching retirement age also.[clarification needed] The breakdown in the more well known countries is as follows: Europe, Northern America, Australia, New Zealand, and Japan has increased from 8 percent in the 1950s to 14 percent in 2000, and is predicted to reach 26 percent in 2050. The reason for these high percentages is a result of a decline in the death and fertility rates.[73]

A worker who starts benefits before normal retirement age has their benefit reduced based on the number of months before normal retirement age they start benefits. This reduction is 5/9 of 1% for each month up to 36 and then 5/12 of 1% for each additional month. This formula gives an 80% benefit at age 62 for a worker with a normal retirement age of 65, a 75% benefit at age 62 for a worker with a normal retirement age of 66, and a 70% benefit at age 62 for a worker with a normal retirement age of 67.

A worker who delays starting retirement benefits past normal retirement age earns delayed retirement credits that increase their benefit until they reach age 70. These credits are also applied to their widow(er)'s benefit. Children and spouse benefits are not affected by these credits.

The normal retirement age for widow(er) benefits shifts the year-of-birth schedule upward by two years, so that those widow(er)s born before 1940 have age 65 as their normal retirement age.

Spouse's benefit

Any current spouse is eligible, and divorced or former spouses are eligible generally if the marriage lasts for at least 10 years. (Civil marriages of same sex couples are not recognized by OASDI for spousal benefits because the federal DOMA law excludes them for federal recognition.) While it is arithmetically possible for one worker to generate spousal benefits for up to five of his/her spouses that he/she may have, each must be in succession after a proper divorce for each after a marriage of at least ten years. Because age 70 is the latest retirement age, and because no state recognizes marriage before teenage years, there are no more than 5 successive spousal benefits in ten-year intervals. This spousal retirement benefit is half the PIA of the worker; this is different from the spousal survivor benefit, which is the full PIA. The benefit is the product of the PIA, times one half, times the early-retirement factor if the spouse is younger than normal retirement age. There is no increase for starting spousal benefits after normal retirement age. This can occur if there is a married couple in which the younger person is the only worker and is more than 5 years younger. Only after the worker applies for retirement benefits may the non-working spouse apply for spousal retirement benefits.

Note that, since the passage of the Senior Citizens' Freedom to Work Act, in 2000, the spouse and children of a worker who has reached normal retirement age can receive benefits on the worker's record whether the worker is receiving benefits or not. Thus a worker can delay retirement without affecting spousal and children's benefits. The worker may have to begin receipt of benefits, to allow the spousal/children's benefits to begin, and then subsequently suspend his/her own benefits in order to continue the postponement of benefits in exchange for an increased benefit amount.[citation needed]

Widow(er)'s benefits

If a worker covered by Social Security dies, a surviving spouse can receive survivors' benefits. In some instances, survivors' benefits are available even to a divorced spouse. A father or mother with minor or disabled children in his or her care can receive benefits which are not actuarially reduced. The earliest age for a nondisabled widow(er)'s benefit is age 60. The benefit is equal to the worker's full retirement benefit for spouses who are at, or older than, normal retirement age. If the surviving spouse starts benefits before normal retirement age, there is an actuarial reduction.[74] If the worker earned delayed retirement credits by waiting to start benefits after their normal retirement age, the surviving spouse will have those credits applied to their benefit.[citation needed]

Children's benefits

Children of a retired, disabled or deceased worker receive benefits as a "dependent" or "survivor" if they are under the age of 18, or between 18 and 19 and have not yet graduated from high school, or are over the age of 18 and were disabled before the age of 22.[74] In a landmark case, the 8th Circuit U.S. Court of Appeals decided that a child is entitled to survivor benefits even though she was born two years after her father's death, having been conceived by in vitro fertilization.[75]

Disability

A worker who has worked long enough and recently enough (based on "quarters of coverage" within the recent past) to be covered can receive disability benefits. These benefits start after five full calendar months of disability, regardless of his or her age. The eligibility formula requires a certain number of credits (based on earnings) to have been earned overall, and a certain number within the ten years immediately preceding the disability, but with more-lenient provisions for younger workers who become disabled before having had a chance to compile a long earnings history.

The worker must be unable to continue in his or her previous job and unable to adjust to other work, with age, education, and work experience taken into account; furthermore, the disability must be long-term, lasting 12 months, expected to last 12 months, resulting in death, or expected to result in death.[76] As with the retirement benefit, the amount of the disability benefit payable depends on the worker's age and record of covered earnings.

Supplemental Security Income (SSI) uses the same disability criteria as the insured social security disability program, but SSI is not based upon insurance coverage. Instead, a system of means-testing is used to determine whether the claimants' income and net worth fall below certain income and asset thresholds.

Severely disabled children may qualify for SSI. Standards for child disability are different from those for adults.

Disability determination at the Social Security Administration has created the largest system of administrative courts in the United States. Depending on the state of residence, a claimant whose initial application for benefits is denied can request reconsideration or a hearing before an Administrative Law Judge (ALJ). Such hearings sometimes involve participation of an independent vocational expert (VE) or medical expert (ME), as called upon by the ALJ.

Reconsideration involves a re-examination of the evidence and, in some cases, the opportunity for a hearing before a (non-attorney) disability hearing officer. The hearing officer then issues a decision in writing, providing justification for his/her finding. If the claimant is denied at the reconsideration stage, (s)he may request a hearing before an Administrative Law Judge. In some states, SSA has implemented a pilot program that eliminates the reconsideration step and allows claimants to appeal an initial denial directly to an Administrative Law Judge.

Because the number of applications for Social Security is very large (approximately 650,000 applications per year), the number of hearings requested by claimants often exceeds the capacity of Administrative Law Judges. The number of hearings requested and availability of Administrative Law Judges varies geographically across the United States. In some areas of the country, it is possible for a claimant to have a hearing with an Administrative Law Judge within 90 days of his/her request. In other areas, waiting times of 18 months are not uncommon.

After the hearing, the Administrative Law Judge (ALJ) issues a decision in writing. The decision can be Fully Favorable (the ALJ finds the claimant disabled as of the date that (s) he alleges in the application through the present), Partially Favorable (the ALJ finds the claimant disabled at some point, but not as of the date alleged in the application; OR the ALJ finds that the claimant was disabled but has improved), or Unfavorable (the ALJ finds that the claimant was not disabled at all). Claimants can appeal Partially Favorable and Unfavorable decisions to Social Security's Appeals Council, which is in Virginia. The Appeals Council does not hold hearings; it accepts written briefs. Response time from the Appeals Council can range from 12 weeks to more than 3 years.

If the claimant disagrees with the Appeals Council's decision, (s)he can appeal the case in the federal district court for his/her jurisdiction. As in most federal court cases, an unfavorable district court decision can be appealed to the appropriate United States Court of Appeals, and an unfavorable appellate court decision can be appealed to the United States Supreme Court.

Current operation

Joining and quitting

Obtaining a Social Security number for a child is voluntary.[77] Further, there is no general legal requirement that individuals join the Social Security program. Although the Social Security Act itself does not require a person to have a Social Security Number (SSN) to live and work in the United States,[78] the Internal Revenue Code does generally require the use of the social security number by individuals for federal tax purposes:

-

- The social security account number issued to an individual for purposes of section 205(c)(2)(A) of the Social Security Act shall, except as shall otherwise be specified under regulations of the Secretary [of the Treasury or his delegate], be used as the identifying number for such individual for purposes of this title.[79]

Importantly, most parents apply for Social Security numbers for their dependent children in order to [80] include them on their income tax returns as a dependent. Everyone filing a tax return, as taxpayer or spouse, must have a Social Security Number or Taxpayer Identification Number (TIN) since the IRS is unable to process returns or post payments for anyone without an SSN or TIN.

The FICA taxes are imposed on all workers and self-employed persons. Employers are required[81] to report wages for covered employment to Social Security for processing Forms W-2 and W-3. There are some specific wages which are not a part of the Social Security program (discussed below). Internal Revenue Code provisions section 3101 imposes payroll taxes on individuals and employer matching taxes. Section 3102[82] mandates that employers deduct these payroll taxes from workers' wages before they are paid. Generally, the payroll tax is imposed on everyone in employment earning "wages" as defined in 3121 of the Internal Revenue Code.[83] and also taxes[84] net earnings from self-employment.[85]

Trust fund

Main article: Social Security Trust FundSocial Security taxes are paid into the Social Security Trust Fund maintained by the U.S. Treasury (technically, the "Federal Old-Age and Survivors Insurance Trust Fund", as established by ). Current year expenses are paid from current Social Security tax revenues. When revenues exceed expenditures, as they have in most years, the excess is invested in special series, non-marketable U.S. Government bonds, thus the Social Security Trust Fund indirectly finances the federal government's general purpose deficit spending. In 2007, the cumulative excess of Social Security taxes and interest received over benefits paid out stood at $2.2 trillion.[86] The Trust Fund is regarded by some as an accounting trick which holds no economic significance. Others argue that it has specific legal significance because the Treasury securities it holds are backed by the "full faith and credit" of the U.S. government, which has an obligation to repay its debt.

The Social Security Administration's authority to make benefit payments as granted by Congress extends only to its current revenues and existing Trust Fund balance, i.e., redemption of its holdings of Treasury securities. Therefore, Social Security's ability to make full payments once annual benefits exceed revenues depends in part on the federal government's ability to make good on the bonds that it has issued to the Social Security trust funds. As with any other federal obligation, the federal government's ability to repay Social Security is based on the power to tax and the commitment of the Congress to meet its obligations.

In 2009 the Office of the Chief Actuary of the Social Security Administration calculated an unfunded obligation of $15.1 trillion for the Social Security program. The unfunded obligation is the difference between the present value of the cost of Social Security and the present value of the assets in the Trust Fund and the future scheduled tax income of the program. In the Actuarial Note explaining the calculation, the Office of the Chief Actuary wrote that "The term obligation is used in lieu of the term liability, because liability generally indicates a contractual obligation (as in the case of private pensions and insurance) that cannot be altered by the plan sponsor without the agreement of the plan participants."[87][88]

Office of Disability Adjudication and Review (ODAR)

"The Office of Hearings and Appeals (OHA) administers the hearings and appeals program for the Social Security Administration (SSA). Administrative Law Judges (ALJs) conduct hearings and issue decisions. The Appeals Council considers appeals from hearing decisions, and acts as the final level of administrative review for the Social Security Administration."[89] In 2006, OHA was renamed to ODAR.[90]

Benefit payout comparisons

The current formula used in calculating the benefit level (primary insurance amount or PIA) is very progressive so that sizable benefits could be obtained with much less than the thirty five to forty years of covered wages. Workers who spend their entire careers in covered employment would be unfairly treated relative to workers who spend the first half of their careers not covered (as in municipal employment) by OASDI but are covered by an alternative plan. These people who later switch into covered employment would be entitled to both the alternative non OASDI pension (presumably from a state or municipality) and get an Old Age retirement benefit from Social Security. The progressivity of the PIA formula would in effect allow these workers to double dip. Therefore, there are two provisions that mitigate the effect of the double dipping: one for those who obtain OASDI benefits from a spouse who is a covered worker and the other for those who split their careers in covered and noncovered employment. This latter double dip has a claw back factor which starts at maximum at 10 years and grades out to zero at 30 years so that there is no clawback for those with 30 years or more of covered wages. This is to prevent those with abnormally low AIMEs due to few years of covered status from being treated as lifetime (say 44 years) career low wage earners with low AIMEs.

International agreements

People sometimes relocate from one country to another, either permanently or on a limited-time basis. This presents challenges to businesses, governments, and individuals seeking to ensure future benefits or having to deal with taxation authorities in multiple countries. To that end, the Social Security Administration has signed treaties, often referred to as Totalization Agreements, with other social insurance programs in various foreign countries.[91]

Overall, these agreements serve two main purposes. First, they eliminate dual Social Security taxation, the situation that occurs when a worker from one country works in another country and is required to pay Social Security taxes to both countries on the same earnings. Second, the agreements help fill gaps in benefit protection for workers who have divided their careers between the United States and another country.

The following countries have signed totalization agreements with the SSA (and the date the agreement became effective):[92]

- Italy (November 1, 1978)

- Germany (December 1, 1979)

- Switzerland (November 1, 1980)

- Belgium (July 1, 1984)

- Norway (July 1, 1984)

- Canada (August 1, 1984)

- United Kingdom (January 1, 1985)

- Sweden (January 1, 1987)

- Spain (April 1, 1988)

- France (July 1, 1988)

- Portugal (August 1, 1989)

- Netherlands (November 1, 1990)

- Austria (November 1, 1991)

- Finland (November 1, 1992)

- Ireland (September 1, 1993)

- Luxembourg (November 1, 1993)

- Greece (September 1, 1994)

- South Korea (April 1, 2001)

- Chile (December 1, 2001)

- Australia (October 1, 2002)

- Japan (October 1, 2005)

- Denmark (October 1, 2008)

- Czech Republic (January 1, 2009)

- Poland (March 1, 2009)

- Mexico (Signed on June 29, 2004, but not yet in effect)

Social Security number

Main article: Social Security numberA side effect of the Social Security program in the United States has been the near-universal adoption of the program's identification number, the Social Security number, as the national identification number in the United States. The social security number, or SSN, is issued pursuant to section 205(c)(2) of the Social Security Act, codified as . The government originally stated that the SSN would not be a means of identification, but currently a multitude of U.S. entities use the Social Security number as a personal identifier. These include government agencies such as the Internal Revenue Service, the military (which prints it on service members' dog tags and uses it in a number of ways to identify personnel, including the name, rank and "serial number" one would furnish the enemy as a POW) as well as private agencies such as banks, colleges and universities, health insurance companies, and employers.

The Social Security Administration admits that the Social Security Act does not require a person to have a Social Security Number to live and work in the United States, nor does it require an SSN simply for the purpose of having one.[78]

The Privacy Act of 1974 was in part intended to limit usage of the Social Security number as a means of identification. Paragraph (1) of subsection (a) of section 7 of the Privacy Act, an uncodified provision, states in part:

-

- (1) It shall be unlawful for any Federal, State or local government agency to deny to any individual any right, benefit, or privilege provided by law because of such individual's refusal to disclose his social security account number.

However, paragraph (2) of subsection (a) of section 7 of the Privacy Act provides in part:

-

- (2) the provisions of paragraph (1) of this subsection shall not apply with respect to –

-

-

- (A) any disclosure which is required by Federal statute, or

-

-

-

- (B) the disclosure of a social security number to any Federal, State, or local agency maintaining a system of records in existence and operating before January 1, 1975, if such disclosure was required under statute or regulation adopted prior to such date to verify the identity of an individual.[93]

-

The exceptions under section 7 of the Privacy Act include the Internal Revenue Code requirement that social security numbers be used as taxpayer identification numbers for individuals.[94]

Demographic and revenue projections

In each year since 1982, OASDI tax receipts, interest payments and other income have exceeded benefit payments and other expenditures, for example by more than $150 billion in 2004.[95] As the "baby boomers" move out of the work force and into retirement, however, expenses will come to exceed tax receipts and then, after several more years, will exceed all system income, including interest. At that point the system will begin drawing on its Treasury Notes, and will continue to pay benefits at the current levels until the Trust Fund is exhausted. At that point, benefits will be reduced to about three-fourths of current levels unless additional revenue is found.

In 2005, this exhaustion of the Trust Fund was projected to occur in 2041 (by the Social Security Administration[96]) or 2052 (by the Congressional Budget Office[97]). Thereafter, however, the projection for the date of this event was moved up by a few years after the recession worsened the system's financial picture. The 2011 OASDI Trustees Report stated:

Annual cost exceeded non-interest income in 2010 and is projected to continue to be larger throughout the remainder of the 75-year valuation period. Nevertheless, from 2010 through 2022, total trust fund income, including interest income, is more than is necessary to cover costs, so trust fund assets will continue to grow during that time period. Beginning in 2023, trust fund assets will diminish until they become exhausted in 2036. Non-interest income is projected to be sufficient to support expenditures at a level of 77 percent of scheduled benefits after trust fund exhaustion in 2036, and then to decline to 74 percent of scheduled benefits in 2085.[98]

In 2007, the Social Security Trustees suggested that either the payroll tax could increase to 16.41 percent in 2041 and steadily increased to 17.60 percent in 2081 or a cut in benefits by 25 percent in 2041 and steadily increased to an overall cut of 30 percent in 2081.[99]

The Social Security Administration projects that the demographic situation will stabilize. The cash flow deficit in the Social Security system will have leveled off as a share of the economy. This projection has come into question. Some demographers argue that life expectancy will improve more than projected by the Social Security Trustees, a development that would make solvency worse. Some economists believe future productivity growth will be higher than the current projections by the Social Security Trustees. In this case, the Social Security shortfall would be smaller than currently projected.

- Tables published by the government's National Center for Health Statistics show that life expectancy at birth was 47.3 years in 1900, rose to 68.2 by 1950 and reached 77.3 in 2002. The latest annual report of the Social Security trustees projects that life expectancy will increase just six years in the next seven decades, to 83 in 2075. A separate set of projections, by the Census Bureau, shows more rapid growth.

("Social Security Underestimates Future Life Spans, Critics Say"[100][dead link]) The Census Bureau projection is that the longer life spans projected for 2075 by the Social Security Administration will be reached in 2050. Other experts, however, think that the past gains in life expectancy cannot be repeated, and add that the adverse effect on the system's finances may be partly offset if health improvements induce people to stay in the workforce longer.

Actuarial science, of the kind used to project the future solvency of social security, is by nature inexact. The SSA actually makes three predictions: optimistic, midline, and pessimistic (until the late 1980s it made 4 projections). The Social Security crisis that was developing prior to the 1983 reforms resulted from midline projections that turned out to be too optimistic. It has been argued that the overly pessimistic projections of the mid to late 1990s were partly the result of the low economic growth (according to actuary David Langer) assumptions which resulted in the projected exhaustion date being pushed back (from 2028 to 2042) with each successive Trustee's report.[citation needed] During the heavy-boom years of the '90s, the midline projections were too pessimistic. Obviously, projecting out 75 years is a significant challenge and, as such, the actual situation might be much better or much worse than predicted.

The Social Security Advisory Board has on three occasions since 1999 appointed a Technical Advisory Panel to review the methods and assumptions used in the annual projections for the Social Security trust funds. The most recent report of the Technical Advisory Panel, released in June 2008 with a copyright date of October 2007, includes a number of recommendations for improving the Social Security projections.[101][102]

Increased spending for Social Security will occur at the same time as increases in Medicare, as a result of the aging of the baby boomers. One projection illustrates the relationship between the two programs:

- From 2004 to 2030, the combined spending on Social Security and Medicare is expected to rise from 7% of national income (gross domestic product) to 13%. Two-thirds of the increase occurs in Medicare.[103]

Online benefits estimate

On July 22, 2008 the Social Security Administration introduced a new online benefits estimator.[104][105] A worker who has enough Social Security credits to qualify for benefits, but who is not currently receiving benefits on his or her own Social Security record and who is not a Medicare beneficiary, can obtain an estimate of the retirement benefit that will be provided, for different assumptions about age at retirement.

Taxation

Tax on wages and self-employment income

Benefits are funded by taxes imposed on wages of employees and self-employed persons. As explained below, in the case of employment, the employer and employee are each responsible for one half of the Social Security tax, with the employee's half being withheld from the employee's pay check. In the case of self-employed persons (i.e., independent contractors), the self-employed person is responsible for the entire amount of Social Security tax.

The Federal Insurance Contributions Act (FICA) (codified in the Internal Revenue Code) imposes a Social Security withholding tax equal to 6.20% of the gross wage amount, up to but not exceeding the Social Security Wage Base ($97,500 for 2007; $102,000 for 2008; and $106,800 for 2009, 2010, and 2011). The same 6.20% tax is imposed on employers. For 2011, the employee's contribution was reduced to 4.2%, while the employer's portion remained at 6.2%.[106] For each calendar year for which the worker is assessed the FICA contribution, the SSA credits those wages as that year's covered wages. The income cutoff is adjusted yearly for inflation and other factors.

A separate payroll tax of 1.45% of an employee's income is paid directly by the employer, and an additional 1.45% deducted from the employee's paycheck, yielding a total tax rate of 2.90%. There is no maximum limit on this portion of the tax. This portion of the tax is used to fund the Medicare program, which is primarily responsible for providing health benefits to retirees.

The combined tax rate of these two federal programs was 15.30% (7.65% paid by the employee and 7.65% paid by the employer) and dropped to 13.30% (5.65% paid by the employee and 7.65% paid by the employer) in 2011.

For self-employed workers (who technically are not employees and are deemed not to be earning "wages" for Federal tax purposes), the self-employment tax, imposed by the Self-Employment Contributions Act of 1954, codified as Chapter 2 of Subtitle A of the Internal Revenue Code, 26 U.S.C. §§ 1401–1403, is 15.3% of "net earnings from self-employment."[107] In essence, a self-employed individual pays both the employee and employer share of the tax, although half of the self-employment tax (the "employer share") is deductible when calculating the individual's federal income tax.[108][109]

If an employee has overpaid payroll taxes by having more than one job or switching jobs during the year, the excess taxes will be refunded when the employee files his federal income tax return. Any excess taxes paid by employers, however, are not refundable to the employers.

Wages not subject to tax

Workers are not required to pay Social Security taxes on wages from certain types of work:[110]

- Wages received by certain state or local government workers participating in their employers' alternative retirement system.

- Net annual earnings from self-employment of less than $400.

- Wages received for service as an election worker, if less than $1,400 a year (in 2008).

- Wages received for working as a household employee, if less than $1,700 per year (in 2009–2010).

- Wages received by college students working under Federal Work Study programs, graduate students receiving stipends while working as teaching assistants, research assistants, or on fellowships, and most postdoctoral researchers. Eliminated starting January 2011.

- Earnings received for serving as a minister (or for similar religious service) if the person has a conscientious objection to public insurance because of personal religious considerations, but only for "qualified services" performed for a religious organization.

- Other minor exceptions.

Federal income taxation of benefits

The benefits received by retirees were not originally taxed as income in the year of receipt. Beginning in tax year 1984, with the Reagan-era reforms to repair the system's projected insolvency, retirees with incomes over $25,000 (in the case of married persons filing separately who did not live with the spouse at any time during the year, and for persons filing as "single"), or with combined incomes over $32,000 (if married filing jointly) or, in certain cases, any income amount (if married filing separately from the spouse in a year in which the taxpayer lived with the spouse at any time) generally saw part of the retiree benefits subject to Federal income tax. In 1984, the portion of the benefits potentially subject to tax was 50%.[111] Under the Deficit Reduction Act of 1993, the portion of benefits potentially subject to tax was increased to 85% beginning with the 1994 tax year.[112]

Criticism of the program

Claim that it discriminates against the poor and the middle class

Critics, such as libertarian Nobel Laureate economist Milton Friedman, say that Social Security redistributes wealth from the poor to the wealthy.[113][114] Workers must pay 12.4 percent, including a 6.2 percent employer contribution, on their wages below the Social Security Wage Base ($106,800, in 2010), but no tax on income in excess of this amount.[115] Therefore, high earners pay a lower percentage of their total income because of the income caps; because of this, payroll taxes are often viewed as being regressive. Furthermore, wealthier individuals generally have higher life expectancies and thus may expect to receive larger benefits for a longer period than poorer taxpayers.[116] A single individual who dies before age 62, who is more likely to be poor, receives no retirement benefits despite his years of paying Social Security tax. On the other hand, an individual who lives to age 100, who is more likely to be wealthy, is guaranteed payments that are more than he paid into the system.[117] An NBER volume edited by Martin Feldstein and Jeffrey Liebman called The Distributional Aspects of Social Security points out that members of racial minorities with lower than average life expectancies and lower than average rates of marriage may also suffer from the program on average.

Supporters of Social Security say that despite its regressive tax formula, Social Security benefits are calculated using a progressive benefit formula that replaces a much higher percentage of low-income workers' pre-retirement income than that of higher-income workers (although these low-income workers pay a higher percentage of their pre-retirement income).[118] They also point to numerous studies that show that, relative to high-income workers, Social Security disability and survivor benefits paid on behalf of low-income workers more than offset any retirement benefits that may be lost because of shorter life expectancy.[119][120][121] Other research asserts that survivor benefits, allegedly an offset, actually exacerbate the problem because survivor benefits are denied to single individuals, including widow(er)s married less than nine months (except in certain situations),[122] divorced widow(er)s married less than 10 years,[123] and co-habiting or same-sex couples, unless they are legally married in their state of residence.[116][124][125][126][127] Unmarried individuals tend to be less wealthy and minorities.[128]

Claim that politicians exempted themselves from the tax

Critics of Social Security have said that the politicians who created Social Security exempted themselves from having to pay the Social Security tax.[129] Indeed, when the federal government created Social Security, all federal employees, including the President and members of Congress, were exempt from having to pay the Social Security tax, and they received no Social Security benefits. This law was changed by the Social Security Amendments of 1983, which brought within the Social Security system all members of Congress, the President and the Vice President, federal judges, and certain executive-level political appointees, as well as all federal employees hired in any capacity on or after January 1, 1984.[130] Many state and local government workers, however, are exempt from Social Security taxes because they contribute instead to alternative retirement systems set up by their employers.[131]

Claim that the government lied about the maximum tax

George Mason University economics professor Walter E. Williams claimed that the federal government has broken its own promise regarding the maximum Social Security tax.[132] Williams used data from the federal government to back up his claim.

According to a 1936 pamphlet on the Social Security website, the federal government promised the following maximum level of taxation for Social Security, "... beginning in 1949, twelve years from now, you and your employer will each pay 3 cents on each dollar you earn, up to $3,000 a year. That is the most you will ever pay."[133]

However, according to the Social Security website, by the year 2008, the tax rate was 6.2% each for the employer and employee, and the maximum income level that was subject to the tax was $102,000 raising the bar to $6,324 maximum contribution by both employee and employer (total $12,648).[134]

In 2005, Williams wrote, "Had Congress lived up to those promises, where $3,000 was the maximum earnings subject to Social Security tax, controlling for inflation, today's $50,000-a-year wage earner would pay about $700 in Social Security taxes, as opposed to the more than $3,000 that he pays today." [132]

According to the Social Security website, "The tax rate in the original 1935 law was 1% each on the employer and the employee, on the first $3,000 of earnings. This rate was increased on a regular schedule in four steps so that by 1949 the rate would be 3% each on the first $3,000. The figure was never $1,400, and the rate was never fixed for all time at 1%."[135]

Claim that it gives a low rate of return

Critics of Social Security [136] claim that it gives a low rate of return, compared to what is obtained through private retirement accounts. For example, critics point out [136] that under the Social Security laws as they existed at that time, several thousand employees of Galveston County, Texas were allowed to opt out of the Social Security program in the early 1980s, and have their money placed in a private retirement plan instead. While employees who earned $50,000 per year would have collected $1,302 per month in Social Security benefits, the private plan paid them $6,843 per month. While employees who earned $20,000 per year would have collected $775 per month in Social Security benefits, the private plan paid them $2,740 per month, at interest rates prevailing in 1996.[136] While some advocates of privatization of Social Security point to the Galveston pension plan as a model for Social Security reform, critics point to a GAO report[137] to the House Ways and Means Committee, which indicates that, for low and middle income employees, particularly those with shorter work histories, the outcome may be less favorable.

Claim that it is a Ponzi scheme

Critics have drawn parallels between Social Security and Ponzi schemes,[138][139][140] e.g.:

...the vast majority of the money you pay in Social Security taxes is not invested in anything. Instead, the money you pay into the system is used to pay benefits to those "early investors" who are retired today. When you retire, you will have to rely on the next generation of workers behind you to pay the taxes that will finance your benefits.As with Ponzi’s scheme, this turns out to be a very good deal for those who got in early. The very first Social Security recipient, Ida Mae Fuller of Vermont, paid just $44 in Social Security taxes, but the long-lived Mrs. Fuller collected $20,993 in benefits. Such high returns were possible because there were many workers paying into the system and only a few retirees taking benefits out of it. In 1950, for instance, there were 16 workers supporting every retiree. Today, there are just over three. By around 2030, we will be down to just two.

As with Ponzi’s scheme, when the number of new contributors dries up, it will become impossible to continue to pay the promised benefits. Those early windfall returns are long gone. When today’s young workers retire, they will receive returns far below what private investments could provide.[141]—Michael TannerPaul Krugman has also echoed this 'Ponzi Scheme' allegation. Commenting on the redistributionary nature of Social Security, Krugman once wrote "Social Security is structured from the point of view of the recipients as if it were an ordinary retirement plan: what you get out depends on what you put in. So it does not look like a redistributionist scheme. In practice it has turned out to be strongly redistributionist, but only because of its Ponzi game aspect, in which each generation takes more out than it put in. Well, the Ponzi game will soon be over, thanks to changing demographics, so that the typical recipient henceforth will get only about as much as he or she put in (and today's young may well get less than they put in)." [142]

One criticism of the analogy is that while Ponzi schemes and Social Security have similar structures (in particular, a sustainability problem when the number of new people paying in is declining), they have different transparencies. In a Ponzi scheme the fact there is no return generating mechanism beyond just contributions from new entrants is obscured[143] whereas Social Security payouts have always been openly underwritten by incoming tax revenue.[144] Private sector Ponzi schemes cannot be sustained indefinitely, whereas Social Security's benefits can theoretically always be sustained by raising taxes on new participants and reducing promised payouts. Because of these and other issues, Robert E. Wright calls Social Security a "quasi" pyramid scheme in his book, Fubarnomics.

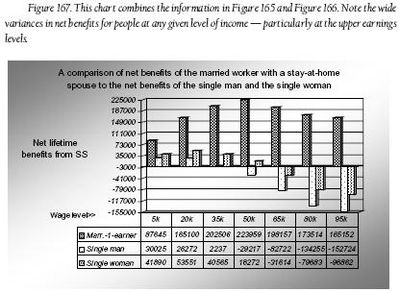

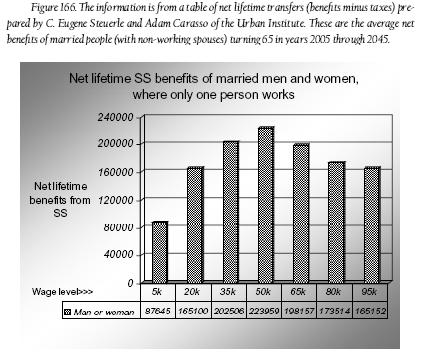

Estimated net Social Security benefits under differing circumstances

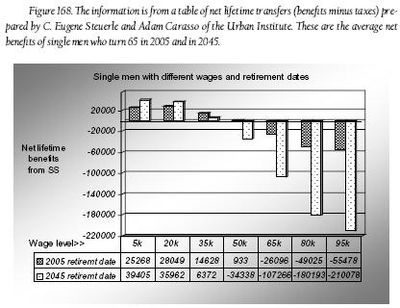

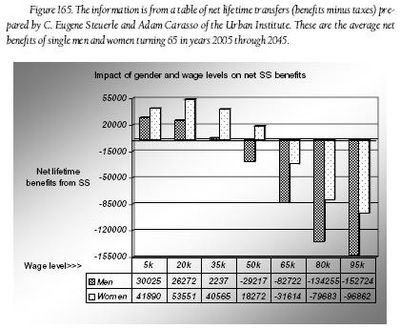

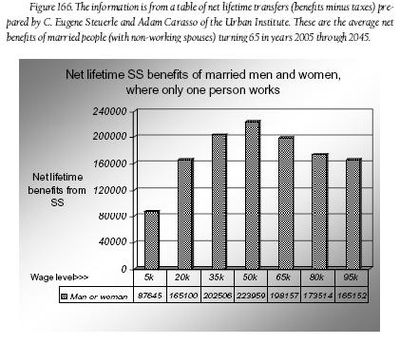

Single men with different wages and retirement dates