- Mortgage loan

-

"Mortgage" redirects here. For other uses, see Mortgage (disambiguation).

Finance Government spending:

Government final consumption expenditure

Warrant of payment

Government operations

Redistribution of wealth

Transfer payment

Government revenue:

Taxation

Deficit spending

Government budget

Government budget deficit

Government debt

Non-tax revenueProfessional certification in financial services

Accounting scandalsA mortgage loan is a loan secured by real property through the use of a mortgage note which evidences the existence of the loan and the encumbrance of that realty through the granting of a mortgage which secures the loan. However, the word mortgage alone, in everyday usage, is most often used to mean mortgage loan.

A home buyer or builder can obtain financing (a loan) either to purchase or secure against the property from a financial institution, such as a bank, either directly or indirectly through intermediaries. Features of mortgage loans such as the size of the loan, maturity of the loan, interest rate, method of paying off the loan, and other characteristics can vary considerably.

In many jurisdictions, though not all (Bali, Indonesia being one exception[1]), it is normal for home purchases to be funded by a mortgage loan. Few individuals have enough savings or liquid funds to enable them to purchase property outright. In countries where the demand for home ownership is highest, strong domestic markets have developed.

The word mortgage is a Law French term meaning "dead pledge," apparently meaning that the pledge ends (dies) either when the obligation is fulfilled or the property is taken through foreclosure.[2]

Contents

Mortgage loan basics

Basic concepts and legal regulation

According to Anglo-American property law, a mortgage occurs when an owner (usually of a fee simple interest in realty) pledges his or her interest (right to the property) as security or collateral for a loan. Therefore, a mortgage is an encumbrance (limitation) on the right to the property just as an easement would be, but because most mortgages occur as a condition for new loan money, the word mortgage has become the generic term for a loan secured by such real property.[3]

As with other types of loans, mortgages have an interest rate and are scheduled to amortize over a set period of time, typically 30 years. All types of real property can be, and usually are, secured with a mortgage and bear an interest rate that is supposed to reflect the lender's risk.

Mortgage lending is the primary mechanism used in many countries to finance private ownership of residential and commercial property (see commercial mortgages). Although the terminology and precise forms will differ from country to country, the basic components tend to be similar:

- Property: the physical residence being financed. The exact form of ownership will vary from country to country, and may restrict the types of lending that are possible.

- Mortgage: the security interest of the lender in the property, which may entail restrictions on the use or disposal of the property. Restrictions may include requirements to purchase home insurance and mortgage insurance, or pay off outstanding debt before selling the property.

- Borrower: the person borrowing who either has or is creating an ownership interest in the property.

- Lender: any lender, but usually a bank or other financial institution. Lenders may also be investors who own an interest in the mortgage through a mortgage-backed security. In such a situation, the initial lender is known as the mortgage originator, which then packages and sells the loan to investors. The payments from the borrower are thereafter collected by a loan servicer.[4]

- Principal: the original size of the loan, which may or may not include certain other costs; as any principal is repaid, the principal will go down in size.

- Interest: a financial charge for use of the lender's money.

- Foreclosure or repossession: the possibility that the lender has to foreclose, repossess or seize the property under certain circumstances is essential to a mortgage loan; without this aspect, the loan is arguably no different from any other type of loan.

Many other specific characteristics are common to many markets, but the above are the essential features. Governments usually regulate many aspects of mortgage lending, either directly (through legal requirements, for example) or indirectly (through regulation of the participants or the financial markets, such as the banking industry), and often through state intervention (direct lending by the government, by state-owned banks, or sponsorship of various entities). Other aspects that define a specific mortgage market may be regional, historical, or driven by specific characteristics of the legal or financial system.

Mortgage loans are generally structured as long-term loans, the periodic payments for which are similar to an annuity and calculated according to the time value of money formulae. The most basic arrangement would require a fixed monthly payment over a period of ten to thirty years, depending on local conditions. Over this period the principal component of the loan (the original loan) would be slowly paid down through amortization. In practice, many variants are possible and common worldwide and within each country.

Lenders provide funds against property to earn interest income, and generally borrow these funds themselves (for example, by taking deposits or issuing bonds). The price at which the lenders borrow money therefore affects the cost of borrowing. Lenders may also, in many countries, sell the mortgage loan to other parties who are interested in receiving the stream of cash payments from the borrower, often in the form of a security (by means of a securitization).

Mortgage lending will also take into account the (perceived) riskiness of the mortgage loan, that is, the likelihood that the funds will be repaid (usually considered a function of the creditworthiness of the borrower); that if they are not repaid, the lender will be able to foreclose and recoup some or all of its original capital; and the financial, interest rate risk and time delays that may be involved in certain circumstances.

Mortgage loan types

There are many types of mortgages used worldwide, but several factors broadly define the characteristics of the mortgage. All of these may be subject to local regulation and legal requirements.

- Interest: interest may be fixed for the life of the loan or variable, and change at certain pre-defined periods; the interest rate can also, of course, be higher or lower.

- Term: mortgage loans generally have a maximum term, that is, the number of years after which an amortizing loan will be repaid. Some mortgage loans may have no amortization, or require full repayment of any remaining balance at a certain date, or even negative amortization.

- Payment amount and frequency: the amount paid per period and the frequency of payments; in some cases, the amount paid per period may change or the borrower may have the option to increase or decrease the amount paid.

- Prepayment: some types of mortgages may limit or restrict prepayment of all or a portion of the loan, or require payment of a penalty to the lender for prepayment.

The two basic types of amortized loans are the fixed rate mortgage (FRM) and adjustable-rate mortgage (ARM) (also known as a floating rate or variable rate mortgage). In many countries (such as the United States), floating rate mortgages are the norm and will simply be referred to as mortgages. Combinations of fixed and floating rate are also common, whereby a mortgage loan will have a fixed rate for some period, and vary after the end of that period.

- In a fixed rate mortgage, the interest rate, and hence periodic payment, remains fixed for the life (or term) of the loan. Therefore the payment is fixed, although ancillary costs (such as property taxes and insurance) can and do change. For a fixed rate mortgage, payments for principal and interest should not change over the life of the loan,

- In an adjustable rate mortgage, the interest rate is generally fixed for a period of time, after which it will periodically (for example, annually or monthly) adjust up or down to some market index. Adjustable rates transfer part of the interest rate risk from the lender to the borrower, and thus are widely used where fixed rate funding is difficult to obtain or prohibitively expensive. Since the risk is transferred to the borrower, the initial interest rate may be from 0.5% to 2% lower than the average 30-year fixed rate; the size of the price differential will be related to debt market conditions, including the yield curve.

The charge to the borrower depends upon the credit risk in addition to the interest rate risk. The mortgage origination and underwriting process involves checking credit scores, debt-to-income, downpayments, and assets. Jumbo mortgages and subprime lending are not supported by government guarantees and face higher interest rates. Other innovations described below can affect the rates as well.

Mortgage underwriting

Main article: Mortgage underwritingLoan to value and downpayments

Main article: Loan-to-value ratioUpon making a mortgage loan for the purchase of a property, lenders usually require that the borrower make a downpayment; that is, contribute a portion of the cost of the property. This downpayment may be expressed as a portion of the value of the property (see below for a definition of this term). The loan to value ratio (or LTV) is the size of the loan against the value of the property. Therefore, a mortgage loan in which the purchaser has made a downpayment of 20% has a loan to value ratio of 80%. For loans made against properties that the borrower already owns, the loan to value ratio will be imputed against the estimated value of the property.

The loan to value ratio is considered an important indicator of the riskiness of a mortgage loan: the higher the LTV, the higher the risk that the value of the property (in case of foreclosure) will be insufficient to cover the remaining principal of the loan.

Value: appraised, estimated, and actual

Since the value of the property is an important factor in understanding the risk of the loan, determining the value is a key factor in mortgage lending. The value may be determined in various ways, but the most common are:

- Actual or transaction value: this is usually taken to be the purchase price of the property. If the property is not being purchased at the time of borrowing, this information may not be available.

- Appraised or surveyed value: in most jurisdictions, some form of appraisal of the value by a licensed professional is common. There is often a requirement for the lender to obtain an official appraisal.

- Estimated value: lenders or other parties may use their own internal estimates, particularly in jurisdictions where no official appraisal procedure exists, but also in some other circumstances.

Payment and debt ratios

In most countries, a number of more or less standard measures of creditworthiness may be used. Common measures include payment to income (mortgage payments as a percentage of gross or net income); debt to income (all debt payments, including mortgage payments, as a percentage of income); and various net worth measures. In many countries, credit scores are used in lieu of or to supplement these measures. There will also be requirements for documentation of the creditworthiness, such as income tax returns, pay stubs, etc; the specifics will vary from location to location.

Some lenders may also require a potential borrower have one or more months of "reserve assets" available. In other words, the borrower may be required to show the availability of enough assets to pay for the housing costs (including mortgage, taxes, etc.) for a period of time in the event of the job loss or other loss of income.

Many countries have lower requirements for certain borrowers, or "no-doc" / "low-doc" lending standards that may be acceptable in certain circumstances.

Standard or conforming mortgages

Many countries have a notion of standard or conforming mortgages that define a perceived acceptable level of risk, which may be formal or informal, and may be reinforced by laws, government intervention, or market practice. For example, a standard mortgage may be considered to be one with no more than 70-80% LTV and no more than one-third of gross income going to mortgage debt.

A standard or conforming mortgage is a key concept as it often defines whether or not the mortgage can be easily sold or securitized, or, if non-standard, may affect the price at which it may be sold. In the United States, a conforming mortgage is one which meets the established rules and procedures of the two major government-sponsored entities in the housing finance market (including some legal requirements). In contrast, lenders who decide to make nonconforming loans are exercising a higher risk tolerance and do so knowing that they face more challenge in reselling the loan. Many countries have similar concepts or agencies that define what are "standard" mortgages. Regulated lenders (such as banks) may be subject to limits or higher risk weightings for non-standard mortgages. For example, banks and mortgage brokerages in Canada face restrictions on lending more than 80% of the property value; beyond this level, mortgage insurance is generally required.[5]

Foreign currency mortgage

In some countries with currencies that tend to depreciate, foreign currency mortgages are common, enabling lenders to lend in a stable foreign currency, whilst the borrower takes on the currency risk that the currency will depreciate and they will therefore need to convert higher amounts of the domestic currency to repay the loan.

Repaying the mortgage

In addition to the two standard means of setting the cost of a mortgage loan (fixed at a set interest rate for the term, or variable relative to market interest rates), there are variations in how that cost is paid, and how the loan itself is repaid. Repayment depends on locality, tax laws and prevailing culture. There are also various mortgage repayment structures to suit different types of borrower.

Capital and interest

The most common way to repay a secured mortgage loan is to make regular payments of the capital (also called the principal) and interest over a set term.[6] This is commonly referred to as (self) amortization in the U.S. and as a repayment mortgage in the UK. A mortgage is a form of annuity (from the perspective of the lender), and the calculation of the periodic payments is based on the time value of money formulas. Certain details may be specific to different locations: interest may be calculated on the basis of a 360-day year, for example; interest may be compounded daily, yearly, or semi-annually; prepayment penalties may apply; and other factors. There may be legal restrictions on certain matters, and consumer protection laws may specify or prohibit certain practices.

Depending on the size of the loan and the prevailing practice in the country the term may be short (10 years) or long (50 years plus). In the UK and U.S., 25 to 30 years is the usual maximum term (although shorter periods, such as 15-year mortgage loans, are common). Mortgage payments, which are typically made monthly, contain a capital (repayment of the principal) and an interest element. The amount of capital included in each payment varies throughout the term of the mortgage. In the early years the repayments are largely interest and a small part capital. Towards the end of the mortgage the payments are mostly capital and a smaller portion interest. In this way the payment amount determined at outset is calculated to ensure the loan is repaid at a specified date in the future. This gives borrowers assurance that by maintaining repayment the loan will be cleared at a specified date, if the interest rate does not change. Some lenders and 3rd parties offer a Bi-weekly mortgage payment program designed to accelerate the payoff of the loan.

Interest only

The main alternative to a capital and interest mortgage is an interest-only mortgage, where the capital is not repaid throughout the term. This type of mortgage is common in the UK, especially when associated with a regular investment plan. With this arrangement regular contributions are made to a separate investment plan designed to build up a lump sum to repay the mortgage at maturity. This type of arrangement is called an investment-backed mortgage or is often related to the type of plan used: endowment mortgage if an endowment policy is used, similarly a Personal Equity Plan (PEP) mortgage, Individual Savings Account (ISA) mortgage or pension mortgage. Historically, investment-backed mortgages offered various tax advantages over repayment mortgages, although this is no longer the case in the UK. Investment-backed mortgages are seen as higher risk as they are dependent on the investment making sufficient return to clear the debt.

Until recently it was not uncommon for interest only mortgages to be arranged without a repayment vehicle, with the borrower gambling that the property market will rise sufficiently for the loan to be repaid by trading down at retirement (or when rent on the property and inflation combine to surpass the interest rate).

No capital or interest

For older borrowers (typically in retirement), it may be possible to arrange a mortgage where neither the capital nor interest is repaid. The interest is rolled up with the capital, increasing the debt each year.

These arrangements are variously called reverse mortgages, lifetime mortgages or equity release mortgages (referring to home equity), depending on the country. The loans are typically not repaid until the borrowers die, hence the age restriction. For further details, see equity release.

Interest and partial capital

In the U.S. a partial amortization or balloon loan is one where the amount of monthly payments due are calculated (amortized) over a certain term, but the outstanding capital balance is due at some point short of that term. In the UK, a part repayment mortgage is quite common, especially where the original mortgage was investment-backed and on moving house further borrowing is arranged on a capital and interest (repayment) basis.

Variations

Graduated payment mortgage loan have increasing costs over time and are geared to young borrowers who expect wage increases over time. Balloon payment mortgages have only partial amortization, meaning that amount of monthly payments due are calculated (amortized) over a certain term, but the outstanding principal balance is due at some point short of that term, and at the end of the term a balloon payment is due. When interest rates are high relative to the rate on an existing seller's loan, the buyer can consider assuming the seller's mortgage.[7] A wraparound mortgage is a form of seller financing that can make it easier for a seller to sell a property. A biweekly mortgage has payments made every two weeks instead of monthly.

Budget loans include taxes and insurance in the mortgage payment;[8] package loans add the costs of furnishings and other personal property to the mortgage. Buydown mortgages allow the seller or lender to pay something similar to mortgage points to reduce interest rate and encourage buyers.[9] Homeowners can also take out equity loans in which they receive cash for a mortgage debt on their house. Shared appreciation mortgages are a form of equity release. In the US, foreign nationals due to their unique situation face Foreign National mortgage conditions.

Flexible mortgages allow for more freedom by the borrower to skip payments or prepay. Offset mortgages allow deposits to be counted against the mortgage loan. in the UK there is also the endowment mortgage where the borrowers pay interest while the principal is paid with a life insurance policy.

Commercial mortgages typically have different interest rates, risks, and contracts than personal loans. Participation mortgages allow multiple investors to share in a loan. Builders may take out blanket loans which cover several properties at once. Bridge loans may be used as temporary financing pending a longer-term loan. Hard money loans provide financing in exchange for the mortgaging of real estate collateral.

Foreclosure and non-recourse lending

Main article: foreclosureIn most jurisdictions, a lender may foreclose the mortgaged property if certain conditions - principally, non-payment of the mortgage loan - occur. Subject to local legal requirements, the property may then be sold. Any amounts received from the sale (net of costs) are applied to the original debt. In some jurisdictions, mortgage loans are non-recourse loans: if the funds recouped from sale of the mortgaged property are insufficient to cover the outstanding debt, the lender may not have recourse to the borrower after foreclosure. In other jurisdictions, the borrower remains responsible for any remaining debt.

In virtually all jurisdictions, specific procedures for foreclosure and sale of the mortgaged property apply, and may be tightly regulated by the relevant government. There are strict or judicial foreclosures and non-judicial foreclosures, also known as power of sale foreclosures. In some jurisdictions, foreclosure and sale can occur quite rapidly, while in others, foreclosure may take many months or even years. In many countries, the ability of lenders to foreclose is extremely limited, and mortgage market development has been notably slower.

Mortgage lending: United States

Main articles: Mortgage industry of the United States and Mortgage underwriting in the United StatesMortgages in the UK

Main article: Mortgage industry of the United KingdomMortgage lending in Continental Europe

Within the European Union, the Covered bonds market volume (covered bonds outstanding) amounted to about EUR 2 trillion at year-end 2007 with Germany, Denmark, Spain, and France each having outstandings above 200,000 EUR million.[10] In German language, Pfandbriefe is the term applied. Pfandbrief-like securities have been introduced in more than 25 European countries – and in recent years also in the U.S. and other countries outside Europe – each with their own unique law and regulations. However, the diffusion of the concept differ: In 2000, the US institutions Fannie Mae and Freddie Mac together reached one per cent of the national population. Furthermore, 87 per cent of their purchased mortgages were granted to borrowers in metropolitan areas with higher income levels. In Europe, a wider market has been achieved: In Denmark, mortgage banks reached 35 per cent of the population in 2002, while the German Bausparkassen achieved widespread regional distribution and more than 30 per cent of the German population concluded a Bauspar contract (as of 2001).[11]

Costs

A study issued by the UN Economic Commission for Europe compared German, US, and Danish mortgage systems. The German Bausparkassen have reported nominal interest rates of approximately 6 per cent per annum in the last 40 years (as of 2004). In addition, they charge administration and service fees (about 1.5 per cent of the loan amount). In the United States, the average interest rates for fixed-rate mortgages in the housing market started in the tens and twenties in the 1980s and have (as of 2004) reached about 6 per cent per annum. However, gross borrowing costs are substantially higher than the nominal interest rate and amounted for the last 30 years to 10.46 per cent. In Denmark, similar to the United States capital market, interest rates have fallen to 6 per cent per annum. A risk and administration fee amounts to 0.5 per cent of the outstanding debt. In addition, an acquisition fee is charged which amounts to one per cent of the principal.[11]

Recent trends

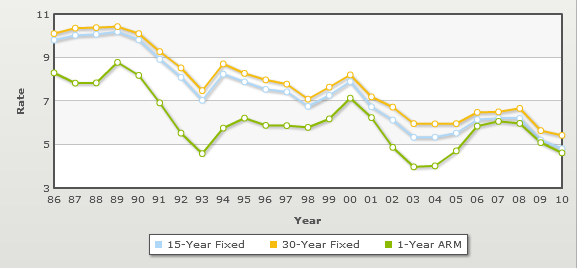

Mortgage Rates Historical Trends 1986 to 2010

Mortgage Rates Historical Trends 1986 to 2010

On July 28, 2008, US Treasury Secretary Henry Paulson announced that, along with four large U.S. banks, the Treasury would attempt to kick start a market for these securities in the United States, primarily to provide an alternative form of mortgage-backed securities.[12] Similarly, in the UK "the Government is inviting views on options for a UK framework to deliver more affordable long-term fixed-rate mortgages, including the lessons to be learned from international markets and institutions".[13]

George Soros's October 10, 2008 Wall Street Journal editorial promoted the Danish mortgage market model.[14] A survey of European Pfandbrief-like products was issued in 2005 by the Bank for International Settlements;[15] the International Monetary Fund in 2007 issued a study of the covered bond markets in Germany and Spain,[16] while the European Central Bank in 2003 issued a study of housing markets, addressing also mortgage markets and providing a two page overview of current mortgage systems in the EU countries.[17]

History

See also: Pfandbrief#History and Danish mortgage marketWhile the idea originated in Prussia in 1769, a Danish act on mortgage credit associations of 1850 enabled the issuing of bonds (Danish: Realkreditobligationer) as a means to refinance mortgage loans. With the German mortgage banks law of 1900, the whole German Empire was given a standardized legal foundation for the emission of Pfandbriefe. An account from the perspective of development economics is available.[18]

Mortgage insurance

Mortgage insurance is an insurance policy designed to protect the mortgagee (lender) from any default by the mortgagor (borrower). It is used commonly in loans with a loan-to-value ratio over 80%, and employed in the event of foreclosure and repossession.

This policy is typically paid for by the borrower as a component to final nominal (note) rate, or in one lump sum up front, or as a separate and itemized component of monthly mortgage payment. In the last case, mortgage insurance can be dropped when the lender informs the borrower, or its subsequent assigns, that the property has appreciated, the loan has been paid down, or any combination of both to relegate the loan-to-value under 80%.

In the event of repossession, banks, investors, etc. must resort to selling the property to recoup their original investment (the money lent), and are able to dispose of hard assets (such as real estate) more quickly by reductions in price. Therefore, the mortgage insurance acts as a hedge should the repossessing authority recover less than full and fair market value for any hard asset.

Islamic mortgages

Main article: Islamic economic jurisprudenceIslamic Sharia law prohibits the payment or receipt of interest, meaning that Muslims cannot use conventional mortgages. However, real estate is far too expensive for most people to buy outright using cash: Islamic mortgages solve this problem by having the property change hands twice. In one variation, the bank will buy the house outright and then act as a landlord. The homebuyer, in addition to paying rent, will pay a contribution towards the purchase of the property. When the last payment is made, the property changes hands.[citation needed]

Typically, this may lead to a higher final price for the buyers. This is because in some countries (such as the United Kingdom and India) there is a Stamp Duty which is a tax charged by the government on a change of ownership. Because ownership changes twice in an Islamic mortgage, a stamp tax may be charged twice. Many other jurisdictions have similar transaction taxes on change of ownership which may be levied. In the United Kingdom, the dual application of Stamp Duty in such transactions was removed in the Finance Act 2003 in order to facilitate Islamic mortgages.[19]

An alternative scheme involves the bank reselling the property according to an installment plan, at a price higher than the original price.

Both of these methods compensate the lender as if they were charging interest, but the loans are structured in a way that in name they are not, and the lender shares the financial risks involved in the transaction with the homebuyer.[citation needed]

See also

Interest rate type Repayment type Continuous: Repayment mortgage / self-amortized · Repayment at term: interest-only mortgage (endowment mortgage) · No repayment: reverse mortgage · Hybrid: balloon payment mortgage · equity release (shared appreciation mortgage)Variable payment Other variations Key concepts Related to the United Kingdom

Related to the United States

- Commercial lender (US) - a term for a lender collateralizing non-residential properties.

- Fixed rate mortgage calculations (USA)

- pre-qualification - U.S. mortgage terminology

- pre-approval - U.S. mortgage terminology

- FHA loan - Relating to the U.S. Federal Housing Administration

- VA loan - Relating to the U.S. Veterans Administration.

- eMortgages

- Location Efficient Mortgage - a type of mortgage for urban areas

- Predatory mortgage lending

Other nations

Legal details

- Deed - legal aspects

- Mechanics lien - a legal concept

- Perfection - applicable legal filing requirements

References

- ^ Sonia Kolesnikov-Jessop (January 29, 2009). "Bali's cash property market keeps prices up". International Herald-Tribune. http://www.iht.com/articles/2009/01/29/properties/rebali.1-395765.php. Retrieved 2009-01-30. "'In Bali, there are no mortgages available, so everyone who owns a house here has paid cash for it,' said Nils Wetterlind, managing director of Tropical Homes, a real estate developer and brokerage based on the island."

- ^ Coke, Edward. Commentaries on the Laws of England. "[I]f he doth not pay, then the Land which is put in pledge upon condition for the payment of the money, is taken from him for ever, and so dead to him upon condition, &c. And if he doth pay the money, then the pledge is dead as to the Tenant"

- ^ "Personal finance glossary". http://www.mortgageloan.com/finance-glossary/mortgage_loan. Retrieved 18 January 2011.

- ^ FTC. Mortgage Servicing: Making Sure Your Payments Count.

- ^ "Who Needs Mortgage Loan Insurance?". Canadian Mortgage and Housing Corporation. http://www.cmhc-schl.gc.ca/en/co/moloin/moloin_002.cfm. Retrieved 2009-01-30.

- ^ "Some info on Homeowner Loans". Loans for people with bad credit. 1 October 2011. http://www.loansforpeoplewithbadcredit.biz/badcreditblog/general-articles/some-info-on-homeowner-loans/. Retrieved 14 October 2011.

- ^ Are Mortgage Assumptions a Good Deal?. Mortgage Professor.

- ^ Cortesi GR. (2003). Mastering Real Estate Principles. p. 371

- ^ Homes: Slow-market savings - the 'buy-down'. CNN Money.

- ^ Covered Bond Outstanding 2007

- ^ a b Housing Finance Systems for countries in Transition - Principles and Examples. United Nations, New York and Geneva, 2005, p. 45

- ^ FDIC Policy Statement on Covered Bonds

- ^ Housing Finance Review: analysis and proposals. HM Treasury, March 2008

- ^ "Denmark offers a model mortgage market"

- ^ Mastroeni, O (2005) Pfandbrief-style products in Europe. Bank for International Settlements (BIS): BIS Papers No 5, 22 Jan 2008

- ^ The Use of Mortgage Covered Bonds, Renzo G. Avesani, Antonio García Pascual,and Elina Ribakova. 2007 International Monetary Fund, IMF Working Paper, WP/07/20, January 2007. 23 p.

- ^ European Central Bank: Structural factors in the EU housing markets, March 2003

- ^ Guinnane TW, Ghatak M (1999) The Economics of Lending with Joint Liability: Theory and Practice. Journal of Development Economics, Vol 60, 195-228, jfr. University of Copenhagen, Department of Economics, Discussion Papers, No 98-16: The Economics of Lending with Joint Liability: Theory and Practice, by Maitreesh Ghatak & Timothy W. Guinnane[dead link]

- ^ Reliefs: Alternative property finance

External links

- Mortgages at the Open Directory Project

- FHA loans (Department of Housing and Urban Development)

- Mortgages: For Home Buyers and Homeowners at USA.gov

- Financial Consumer Agency of Canada

Unsecured debt Credit card debt (cash advance) · Overdraft · Payday loan · Personal loan / Signature loan · moneylender

Secured debt Mortgage loan / Home equity loan / Home equity line of credit · car title loan / logbook loan · tax refund anticipation loan · pawnbrokerDebt management Key concepts Annual Percentage Rate (APR)Categories:

Wikimedia Foundation. 2010.