- History of banking

-

The first banks were the merchants of the ancient world that made loans to farmers and traders that carried goods between cities. The first records of such activity dates back to around 2000 BC in Assyria and Babylonia. Later, in ancient Greece and during the Roman Empire, lenders who were based in temples made loans but also added two important innovations: accepting deposits and changing money. During this period, there is similar evidence of the independent development of lending of money in ancient China and separately in ancient India.

Banking, in the modern sense of the word, can be traced to medieval and early Renaissance Italy, to the rich cities in the north such as Florence, Venice and Genoa. The Bardi and Peruzzi families dominated banking in 14th century Florence, establishing branches in many other parts of Europe.[1] Perhaps the most famous Italian bank was the Medici bank, established by Giovanni Medici in 1397.[2]

The development of banking spread through Europe and a number of important innovations took place in Amsterdam during the Dutch Republic in the 16th century and in London in the 17th century. During the 20th century, developments in telecommunications and computing resulting in major changes to the way banks operated and allowed them to dramatically increase in size and geographic spread. The Late-2000s financial crisis saw significant number of bank failures, including some of the world's largest banks, and much debate about bank regulation.

Contents

Earliest forms of banking

The history of banking is closely related to the history of money but banking transactions probably predate the invention of money. Deposits initially consisted of grain and later other goods including cattle, agricultural implements, and eventually precious metals such as gold, in the form of easy-to-carry compressed plates. Temples and palaces were the safest places to store gold as they were constantly attended and well built. As sacred places, temples presented an extra deterrent to would-be thieves.

Mesopotamia

There are records of loans from the 2nd millennium BC in Babylon that were made by temple priests/monks to merchants. By the time of Hammurabi's Code, dating to ca. 1760 BCE, banking was well enough developed to justify laws governing banking operations.[nb 1]

Egypt

In Egypt, from early times, grain had been used as a form of money in addition to precious metals, and state granaries functioned as banks. When Egypt fell under the rule of a Greek dynasty, the Ptolemies (332-30 BC), the numerous scattered government granaries were transformed into a network of grain banks, centralized in Alexandria where the main accounts from all the state granary banks were recorded. This banking network functioned as a trade credit system in which payments were effected by transfer from one account to another without money passing. In the late 3rd century BC, the barren Aegean island of Delos, known for its magnificent harbor and famous temple of Apollo, became a prominent banking center. As in Egypt, cash transactions were replaced by real credit receipts and payments were made based on simple instructions with accounts kept for each client.

India

In ancient India during the Maurya dynasty (321 to 185 BC), an instrument called adesha was in use, which was an order on a banker desiring him to pay the money of the note to a third person, which corresponds to the definition of a bill of exchange as we understand it today. During the Buddhist period, there was considerable use of these instruments. Merchants in large towns gave letters of credit to one another.[3]

China

In ancient China starting in the Qin Dynasty (221 to 206 BC) the Chinese currency developed with the introduction of standardized coins which allowed the much easier trade across China and led to the development of letters of credit. These letters were issued by merchants that acted in ways that today we would understand as banks.[4]

Greece

Ancient Greece holds further evidence of banking. Greek temples, as well as private and civic entities, conducted financial transactions such as loans, deposits, currency exchange, and validation of coinage.[5] There is evidence too of credit, whereby in return for a payment from a client, a moneylender in one Greek port would write a credit note for the client who could "cash" the note in another city, saving the client the danger of carting coinage with him on his journey. Pythius, who operated as a merchant banker throughout Asia Minor at the beginning of the 5th century BC, is the first individual banker of whom we have records. Many of the early bankers in Greek city-states were metics or foreign residents. Around 371 BC, Pasion, a slave, became the wealthiest and most famous Greek banker, gaining his freedom and Athenian citizenship in the process.

Rome

Gold coin produced by the Roman Imperial Mint

Gold coin produced by the Roman Imperial Mint

In Ancient Rome moneylenders would set up their stalls in the middle of enclosed courtyards called macella on a long bench called a bancu, from which the words banco and bank are derived. As a moneychanger, the merchant at the bancu did not so much invest money as merely convert the foreign currency into the only legal tender in Rome that of the Imperial Mint.[6]

The Roman empire formalized the administrative aspect of banking and instituted greater regulation of financial institutions and financial practices. Charging interest on loans and paying interest on deposits became more highly developed and competitive. The development of Roman banks was limited, however, by the Roman preference for cash transactions. During the reign of the Roman emperor Gallienus (260-268 AD), there was a temporary breakdown of the Roman banking system after the banks rejected the flakes of copper produced by his mints. With the ascent of Christianity, banking became subject to additional restrictions, as the charging of interest was seen as immoral. After the fall of Rome banking temporarily ended in Europe and was not revived until the time of the crusades.[citation needed]

Religious restrictions on interest

Most early religious systems in the ancient Near East, and the secular codes arising from them, did not forbid usury. These societies regarded inanimate matter as alive, like plants, animals and people, and capable of reproducing itself. Hence if you lent 'food money', or monetary tokens of any kind, it was legitimate to charge interest.[7] Food money in the shape of olives, dates, seeds or animals was lent out as early as c. 5000 BCE, if not earlier. Among the Mesopotamians, Hittites, Phoenicians and Egyptians, interest was legal and often fixed by the state.[8]

Judaism

Main articles: Loans and interest in Judaism and Jewish views of poverty, wealth and charityThe Torah and later sections of the Hebrew Bible criticize interest-taking, but interpretations of the Biblical prohibition vary. One common understanding is that Jews are forbidden to charge interest upon loans made to other Jews, but obliged to charge interest on transactions with non-Jews, or Gentiles. However, the Hebrew Bible itself gives numerous examples where this provision was evaded.

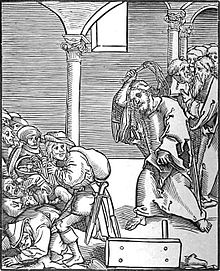

Deuteronomy 23:19 Thou shalt not lend upon interest to thy brother: interest of money, interest of victuals, interest of any thing that is lent upon interest. Deuteronomy 23:20 Unto a foreigner thou mayest lend upon interest; but unto thy brother thou shalt not lend upon interest; that the LORD thy God may bless thee in all that thou puttest thy hand unto, in the land whither thou goest in to possess it.[9] Christ drives the Usurers out of the Temple, a woodcut by Lucas Cranach the Elder in Passionary of Christ and Antichrist.[10]

Christ drives the Usurers out of the Temple, a woodcut by Lucas Cranach the Elder in Passionary of Christ and Antichrist.[10]Israelites were forbidden to charge interest on loans made to other Israelites, but allowed to charge interest on transactions with non-Israelites, as the latter were often amongst the Israelites for the purpose of business anyway, but in general, it was seen as advantageous to avoid getting into debt at all to avoid being bound to someone else. Debt was to be avoided and not used to finance consumption, but only when in need. However, the laws against usury were among the many which the prophets condemn the people for breaking.[11]

Christianity

Main article: UsuryOriginally, the charging of interest known as Usury was banned by Christian churches meaning the charging of interest at any rate banned. This included charging a fee for the use of money, such as at a bureau de change. However over time the charging of interest became acceptable, the term came to be used for interest above the rate allowed by law.

Islam

Main article: RibaIn Islam it is strictly prohibited to take interest; the Quran strictly prohibits lending money on Interest. "O you who have believed, do not consume usury, doubled and multiplied, but fear Allah that you may be successful" (3:130) "and Allah has permitted trade and has forbidden interest" (2:275).

Riba (usury) is forbidden in Islamic economic jurisprudence fiqh. There are two types of riba discussed by Islamic jurists: an increase in capital without any services provided, which is prohibited by the Qur'an, and that prohibited in the Sunnah which comprises commodity exchanges in unequal quantities.

Medieval Europe

Banking in the modern sense of the word can be traced to medieval and early Renaissance Italy, to the rich cities in the north such as Florence, Venice and Genoa.

Emergence of merchant banks

Main article: Merchant bankThe original banks were "merchant banks" which were first invented in the Middle Ages by Italian grain merchants. As the Lombardy merchants and bankers grew in stature based on the strength of the Lombard plains cereal crops, many displaced Jews fleeing Spanish persecution were attracted to the trade. They brought with them ancient practices from the Middle and Far East silk routes. Originally intended for the finance of long trading journeys, these methods were applied to finance the production and trading of grain.

The Jews could not hold land in Italy, so they entered the great trading piazzas and halls of Lombardy, alongside the local traders, and set up their benches to trade in crops. They had one great advantage over the locals. Christians were strictly forbidden the sin of usury, defined as lending at interest (Islam makes similar condemnations of usury). The Jewish newcomers, on the other hand, could lend to farmers against crops in the field, a high-risk loan at what would have been considered usurious rates by the Church; but the Jews were not subject to the Church's dictates.[citation needed] In this way they could secure the grain-sale rights against the eventual harvest. They then began to advance payment against the future delivery of grain shipped to distant ports. In both cases they made their profit from the present discount against the future price. This two-handed trade was time-consuming and soon there arose a class of merchants who were trading grain debt instead of grain.

The Jewish trader performed both financing (credit) and underwriting (insurance) functions. Financing took the form of a crop loan at the beginning of the growing season, which allowed a farmer to develop and manufacture (through seeding, growing, weeding, and harvesting) his annual crop. Underwriting in the form of a crop, or commodity, insurance guaranteed the delivery of the crop to its buyer, typically a merchant wholesaler. In addition, traders performed the merchant function by making arrangements to supply the buyer of the crop through alternative sources—grain stores or alternate markets, for instance—in the event of crop failure. He could also keep the farmer (or other commodity producer) in business during a drought or other crop failure, through the issuance of a crop (or commodity) insurance against the hazard of failure of his crop.

Merchant banking progressed from financing trade on one's own behalf to settling trades for others and then to holding deposits for settlement of "billette" or notes written by the people who were still brokering the actual grain. And so the merchant's "benches" (bank is derived from the Italian for bench, banca, as in a counter) in the great grain markets became centers for holding money against a bill (billette, a note, a letter of formal exchange, later a bill of exchange and later still a cheque).

These deposited funds were intended to be held for the settlement of grain trades, but often were used for the bench's own trades in the meantime. The term bankrupt is a corruption of the Italian banca rotta, or broken bench, which is what happened when someone lost his traders' deposits. Being "broke" has the same connotation.

Crusades

In the 12th century, the need to transfer large sums of money to finance the Crusades stimulated the re-emergence of banking in western Europe. In 1162, King Henry the II levied a tax to support the crusades—the first of a series of taxes levied by Henry over the years with the same objective. The Templars and Hospitallers acted as Henry's bankers in the Holy Land. The Templars' wide flung, large land holdings across Europe also emerged in the 1100–1300 time frame as the beginning of Europe-wide banking, as their practice was to take in local currency, for which a demand note would be given that would be good at any of their castles across Europe, allowing movement of money without the usual risk of robbery while traveling.

Discounting of interest

A sensible manner of discounting interest to the depositors against what could be earned by employing their money in the trade of the bench soon developed; in short, selling an "interest" to them in a specific trade, thus overcoming the usury objection. Once again this merely developed what was an ancient method of financing long-distance transport of goods. Medieval trade fairs, such as the one in Hamburg, contributed to the growth of banking in a curious way: moneychangers issued documents redeemable at other fairs, in exchange for hard currency. These documents could be cashed at another fair in a different country or at a future fair in the same location. If redeemable at a future date, they would often be discounted by an amount comparable to a rate of interest. Eventually, these documents evolved into bills of exchange, which could be redeemed at any office of the issuing banker. These bills made it possible to transfer large sums of money without the complications of hauling large chests of gold and hiring armed guards to protect the gold from thieves.

Foreign exchange contracts

In 1156, in Genoa, occurred the earliest known foreign exchange contract. Two brothers borrowed 115 Genoese pounds and agreed to reimburse the bank's agents in Constantinople the sum of 460 bezants one month after their arrival in that city. In the following century the use of such contracts grew rapidly, particularly since profits from time differences were seen as not infringing canon laws against usury.

Italian bankers

In the middle of the 13th century, groups of Italian Christians, particularly the Cahorsins and Lombards, invented legal fictions to get around the ban on Christian usury;[12] for example, one method of effecting a loan with interest was to offer money without interest, but also require that the loan is insured against possible loss or injury, and/or delays in repayment (see contractum trinius).[12] The Christians effecting these legal fictions became known as the pope's usurers, and reduced the importance of the Jews to European monarchs;[12] later, in the Middle Ages, a distinction was drawn between things which were consumable (such as food and fuel) and those which were not, with usury being permitted on loans involving the latter.[12]

The Bardi and Peruzzi families dominated banking in 14th century Florence, establishing branches in many other parts of Europe.[1] Perhaps the most famous Italian bank was the Medici bank, set up by Giovanni Medici in 1397.[13] Banca Monte dei Paschi di Siena SPA (MPS) Italy, is the oldest surviving bank in the world.

Ironically, the Papal bankers were the most successful of the Western world, though often goods taken in pawn were substituted for interest in the institution termed the Monte di Pietà. Civil war in Florence between the rival Guelph and Ghibelline factions resulted in victory for a group of Guelph merchant families in the city. They took over papal banking monopolies from rivals in nearby Siena and became tax collectors for the Pope throughout Europe.

In 1306, Philip IV expelled Jews from France. In 1307 Philip had the Knights Templar arrested and acquired their wealth, which had become to serve as the unofficial treasury of France. In 1311 he expelled Italian bankers and collected their outstanding credit. In 1327, Avignon had 43 branches of Italian banking houses. In 1347, Edward III of England defaulted on loans. Later there was the bankruptcy of the Peruzzi (1374) and Bardi (1353). The accompanying growth of Italian banking in France was the start of the Lombard moneychangers in Europe, who moved from city to city along the busy pilgrim routes important for trade. Key cities in this period were Cahors, the birthplace of Pope John XXII, and Figeac.

By the later Middle Ages, Christian Merchants who lent money with interest were without opposition, and the Jews lost their privileged position as money-lenders;[12]

After 1400, political forces turned against the methods of the Italian free enterprise bankers. In 1401, King Martin I of Aragon expelled them. In 1403, Henry IV of England prohibited them from taking profits in any way in his kingdom. In 1409, Flanders imprisoned and then expelled Genoese bankers. In 1410, all Italian merchants were expelled from Paris. In 1401, the Bank of Barcelona was founded. In 1407, the Bank of Saint George was founded in Genoa. This bank dominated business in the Mediterranean. In 1403 charging interest on loans was ruled legal in Florence despite the traditional Christian prohibition of usury. Italian banks such as the Lombards, who had agents in the main economic centers of Europe, had been making charges for loans. The lawyer and theologian Lorenzo di Antonio Ridolfi won a case which legalized interest payments by the Florentine government. In 1413, Giovanni di Bicci de’Medici was appointed banker to the pope. In 1440, Gutenberg invented the modern printing press although Europe already knew of the use of paper money in China.

Silver crisis

By the 1390s silver was in short supply all over Europe, except in Venice. The silver mines at Kutná Hora had begun to decline in the 1370s, and finally closed down after being sacked by King Sigismund in 1422. By 1450 almost all of the mints of northwest Europe had closed down for lack of silver. The last money-changer in the major French port of Dieppe went out of business in 1446. In 1455 the Turks overran the Serbian silver mines, and in 1460 captured the last Bosnian mine. As currency became scarce, several Venetian banks failed as did the Strozzi bank of Florence, the second largest in the city.

Spread through Europe

The medieval Italian markets were disrupted by wars and were limited by the fractured nature of the Italian states, so the next developments happened as banking practises spread throughout Europe during the renaissance period. Banking offices were usually located near centers of trade, and in the late 17th century, the largest centers for commerce were the ports of Amsterdam, London, and Hamburg.

Expansion to Germany and Poland

The next generation of bankers arose from migrant Jewish merchants in the great wheat-growing areas of Germany and Poland. Many of these merchants were from the same families who had been part of the development of the banking process in Italy. They also had links with family members who had, centuries before, fled Spain for both Italy and England. As non-agricultural wealth expanded, many families of goldsmiths (another business not prohibited to Jews) also gradually moved into banking.

Berenberg Bank is the oldest private bank in Germany, established in 1590 by Dutch brothers, Hans and Paul Berenberg in Hamburg [14]

Spain and the Ottoman Empire

Halil İnalcik suggests that, in the sixteenth century, Marrano Jews fleeing from Iberia introduced the techniques of European capitalism, banking and even the mercantilist concept of state economy to the Ottoman empire.[15] In the sixteenth century, the leading financiers in Istanbul were Greeks and Jews. Many of the Jewish financiers were Marranos who had fled from Iberia during the period leading up to the expulsion of Jews from Spain. Some of these families brought great fortunes with them.[16] The most notable of the Jewish banking families in the sixteenth century Ottoman Empire was the Marrano banking house of Mendes which moved to and settled in Istanbul in 1552, under the protection of Sultan Suleyman the Magnificent. When Alvaro Mendes arrived in Istanbul in 1588, he is reported to have brought with him 85,000 gold ducats.[17] The Mendès family soon acquired a dominating position in the state finances of the Ottoman Empire and in commerce with Europe.[18]

They thrived in Baghdad during the eighteenth and nineteenth centuries under Ottoman rule, performing critical commercial functions such as moneylending and banking.[19] Like the Armenians, the Jews could engage in necessary commercial activities, such as moneylending and banking, that were proscribed for Moslems under Islamic law.

Emergence of the Court Jew

Main article: Court Jew Joseph Suss Oppenheimer, who served Karl Alexander, Duke of Württemberg

Joseph Suss Oppenheimer, who served Karl Alexander, Duke of WürttembergCourt Jews were Jewish bankers or businessmen who lent money and handled the finances of some of the Christian European noble houses, primarily in the seventeenth and eighteenth centuries.[20] Court Jews were precursors to the modern financier or Secretary of the Treasury.[20] Their jobs included raising revenues by tax farming, negotiating loans, master of the mint, creating new sources for revenue, negotiating loans, float ing debentures, devising new taxes. and supplying the military.[20][21] In addition, the Court Jew acted as personal bankers for nobility: he raised money to cover the noble's personal diplomacy and his extravagances.[21]

Court Jews were skilled administrators and businessmen who received privileges in return for their services. They were most commonly found in Germany, Holland, and Austria, but also in Denmark, England, Hungary, Italy, Poland, Lithuania, Portugal, and Spain.[22][23] According to Dimont, virtually every duchy, principality, and palatinate in the Holy Roman Empire had a Court Jew.[20]

Examples of what would be later called court Jews emerged when local rulers used services of Jewish bankers for short-term loans. They lent money to nobles and in the process gained social influence. Noble patrons of court Jews employed them as financiers, suppliers, diplomats and trade delegates. Court Jews could use their family connections, and connections between each other, to provision their sponsors with, among other things, food, arms, ammunition and precious metals. In return for their services, court Jews gained social privileges, including up to noble status for themselves, and could live outside the Jewish ghettos. Some nobles wanted to keep their bankers in their own courts. And because they were under noble protection, they were exempted from rabbinical jurisdiction. One of the most notable families engaged in this activity was the Rothschild family that created the a banking empire that had branches all over Europe.

Netherlands

Further information: Financial history of the Dutch Republic A painting of the old town hall in Amsterdam where the bank was founded in 1609.

A painting of the old town hall in Amsterdam where the bank was founded in 1609.In the early 1500s in the Dutch Republic in order to protect their large accumulations of cash, people began to depositing their money with "cashiers". These cashiers held the money for a fee. Competition drove cashiers to offer additional services, including paying out money to any person bearing a written order from a depositor to do so; this practise led to the development of cheques.

In the 1600s One of the first measures of the revolutionary Dutch government after breaking away from Spain was "free" or "individual" coinage, where the state would coin any metal delivered to it at no or very small cost. Free coinage was an immediate success. As the seventeenth century began, the Dutch were the driving force behind European commerce. The coins that had legal tender status were often worn and damaged, so it was not easy to exchange them.

To do so, the Bank of Amsterdam (Amsterdamsche Wisselbank) was founded in 1609. Coins were taken in as deposits based not on the face value, but on the real value of their metal weight, with credits, known as bank money, issued against them. And so was created a perfectly uniform currency. This, along with the convenience and security of the new money - and the guarantee of the city of Amsterdam, caused the bank money to trade at an agio, or premium over coins.

The Bank was at first a strictly deposit bank with 100 percent backing, but secretly allowed some depositors to overdraw their accounts as early as 1657 and later provided large loans to the Dutch East India Company and the Municipality of Amsterdam. By 1790 these loans became public and the premium on the bank money disappeared, by the end of that year the Bank virtually admitted insolvency by issuing a notice that silver would be sold to holders of bank money at a 10 percent discount. The City of Amsterdam took the Bank over, and eventually closed it for good in 1819.

Throughout 17th century, precious metals from the New World, Japan and other locales have been channeled into Europe, with corresponding price increases. Thanks to the free coinage, the Bank of Amsterdam, and the heightened trade and commerce, Netherlands attracted even more coin and bullion. These concepts of Fractional-reserve banking and payment systems went on and spread to England and elsewhere.[24]

England

Further information: Banking in the United KingdomThe London Royal Exchange was established in 1565. At that time moneychangers were already called bankers, though the term "bank" usually referred to their offices, and did not carry the meaning it does today. There was also a hierarchical order among professionals; at the top were the bankers who did business with heads of state, next were the city exchanges, and at the bottom were the pawn shops or "Lombard"'s. Some European cities today have a Lombard street where the pawn shop was located.

Advances in the 17th and 18th century

By the end of the 16th century and during the 17th, the traditional banking functions of accepting deposits, moneylending, money changing, and transferring funds were combined with the issuance of bank debt that served as a substitute for gold and silver coins.

New banking practices promoted commercial and industrial growth by providing a safe and convenient means of payment and a money supply more responsive to commercial needs, as well as by "discounting" business debt. By the end of the 17th century, banking was also becoming important for the funding requirements of the relatively new and combative european states. This would lead on to government regulations and the first central banks. The success of the new banking techniques and practices in Amsterdam and also the thriving trade city of Antwerp help spread the concepts and ideas to London and helped the developments elsewhere in Europe.

Goldsmiths of London

The main developers of banking in London were the goldsmiths, who transformed from simple artisans to becoming depositories of gold and silver holdings. Events such at the appropriation of £200,000 of private money by King Charles I from the royal mint, in 1640 caused merchants to lose trust in the existing institutions and drive them to find more trusted alternatives such as the goldsmiths.

The goldsmiths soon found themselves with money for which they had no immediate use, and they began to lend the money out at interest to both the merchants and the government. Finding substantial profit in this business, they began to solicit deposits and pay interest on them. The goldsmiths eventually discovered that the deposit receipts they provided were being passed on from one person to another in lieu of payment in coin, which prompted them to begin lending paper receipts rather than coins. By promoting acceptance of the receipts as a means of payment, the goldsmiths discovered they could lend more than the gold and silver coin they had on hand, a practice that became known as fractional-reserve banking.[25]

Debt as a new kind of money

These practices created a new kind of "money" that was actually debt, that is, goldsmiths' debt rather than silver or gold coin, a commodity that had been regulated and controlled by the monarchy. This development required the acceptance in trade of the goldsmiths' promissory notes, payable on demand. Acceptance in turn required a general belief that coin would be available; and a fractional reserve normally served this purpose. Acceptance also required that the holders of debt be able legally to enforce an unconditional right to payment; it required that the notes (as well as drafts) be negotiable instruments. The concept of negotiability had emerged in fits and starts in European money markets, but it was well developed by the 17th century. Nevertheless, an act of Parliament was required in the early 18th century (1704) to overrule court decisions holding that the gold smiths notes, despite the "customs of "merchants, were not negotiable.[25]

Meanwhile, the credit of the British Crown had been diminished by default in 1672. The monarchy's urgent need for funds at rates lower than those charged by the goldsmiths, and the example of the public Bank of Amsterdam, which had been able to make an ample supply of credit available at low interest rates, led in 1694 to the establishment of the Bank of England. The Bank of England succeeded in raising money for the government at relatively low rates.

Development of central banking

In 18th-century London the Bank of England had a monopoly over corporate banking, and even large partnerships were prohibited. But private banks, though relatively small, personal enterprises, continued to find profitable business in discounting merchants' bills. In the latter half of the century small banks in country towns grew rapidly in number and needed "correspondent" banks in London with which they could deposit and invest funds. The London banks in turn settled accounts in Bank of England notes, and by the end of the century many kept their own deposit accounts with the Bank of England.[25] A structure that led to the development of the concept of a central bank.

Removal of religious restrictions on earning interest

The rise of Protestantism, freed many European Christians from Rome's dictates against usury. In the late 18th century, protestant merchant families began to move into banking, especially in trading countries such as the United Kingdom (Barings), Germany (Schroders) and the Netherlands (Hope & Co.) At the same time, new types of financial activities broadened the scope of banking far beyond its origins. The merchant-banking families dealt in everything from underwriting bonds to originating foreign loans. For instance, bullion trading and bond issuance were two of the specialties of the Rothschilds. In 1803, Barings teamed with Hope & Co. to facilitate the Louisiana Purchase.

19th century

In the nineteenth century, spurred at first by financing required for the Napoleonic wars and then by the explosion of railroads in Europe, banks evolved into large commercial entities, lending to the public, and often publicly traded.[26] Jews were founders and leaders of many of the important early European banks, as well as significant banks in the United States.[20][27][28] Several Jewish bankers became extremely influential, successfully competing with non-Jewish banking houses in the floating of government loans.[29]

Europe

Rothschild family banking businesses pioneered international high finance during the industrialisation of Europe and were instrumental in supporting railway systems across the world and in complex government financing for projects such as the Suez Canal. The family bought up a large proportion of the property in Mayfair, London. Major businesses directly founded by Rothschild family capital include Alliance Assurance (1824) (now Royal & SunAlliance); Chemin de Fer du Nord (1845); Rio Tinto Group (1873); Société Le Nickel (1880) (now Eramet); and Imétal (1962) (now Imerys). The Rothschilds financed the founding of De Beers, as well as Cecil Rhodes on his expeditions in Africa and the creation of the colony of Rhodesia. From the late 1880s onwards, the family controlled the Rio Tinto mining company.[30]

The Japanese government approached the London and Paris families for funding during the Russo-Japanese War. The London consortium's issue of Japanese war bonds would total £11.5 million (at 1907 currency rates).[31]

United States

See also: History of banking in the United States and History of investment banking in the United StatesIn the 19th century, the rise of trade and industry in the US led to powerful new private merchant banks, culminating in J.P. Morgan & Co. During the 20th century, however, the financial world began to outgrow the resources of family-owned and other forms of private-equity banking. Corporations came to dominate the banking business. For the same reasons, merchant banking activities became just one area of interest for modern banks.[32]

Globalisation

In the late 18th century there was a massive growth in the banking industry. Banks played a key role in moving from gold and silver based coinage to paper money, redeemable against the bank's holdings. Within the new system of ownership and investment, the state's role as an economic factor grew substantially.[33]

20th century

The first decade of the 20th century saw the Panic of 1907 in the US, which led to numerous runs on banks and became known as the bankers panic.

1930s Great Depression

Crowd at New York's American Union Bank during a bank run early in the Great Depression.

Crowd at New York's American Union Bank during a bank run early in the Great Depression.During the Crash of 1929 preceding the Great Depression, margin requirements were only 10%.[34] Brokerage firms, in other words, would lend $9 for every $1 an investor had deposited. When the market fell, brokers called in these loans, which could not be paid back. Banks began to fail as debtors defaulted on debt and depositors attempted to withdraw their deposits en masse, triggering multiple bank runs. Government guarantees and Federal Reserve banking regulations to prevent such panics were ineffective or not used. Bank failures led to the loss of billions of dollars in assets.[35] Outstanding debts became heavier, because prices and incomes fell by 20–50% but the debts remained at the same dollar amount. After the panic of 1929, and during the first 10 months of 1930, 744 US banks failed. By April 1933, around $7 billion in deposits had been frozen in failed banks or those left unlicensed after the March Bank Holiday.[36]

Bank failures snowballed as desperate bankers called in loans which the borrowers did not have time or money to repay. With future profits looking poor, capital investment and construction slowed or completely ceased. In the face of bad loans and worsening future prospects, the surviving banks became even more conservative in their lending.[35] Banks built up their capital reserves and made fewer loans, which intensified deflationary pressures. A vicious cycle developed and the downward spiral accelerated. In all, over 9,000 banks failed during the 1930s.

In response many countries significantly increased financial regulation. In the US the Securities and Exchange Commission was established in 1933 and the Glass–Steagall Act was passed which would separate investment banking and commercial banking. This was to try and avoid the more risky investment banking activities from causing bank failures for commercial banks ever again.

World Bank and the development of payment technology

During the post second world war period and with the introduction of the Bretton Woods system in 1944, two organizations were created: the International Monetary Fund (IMF) and the World Bank. Encouraged by these institutions, commercial banks started to lend to sovereign states in the third world. This was at the same time as inflation started to rise in the west. The Gold standard was eventually abandoned in 1971 and a number of the banks were caught out and became bankrupt due to third world country debt defaults.

This was also a time that saw an increasing use of technology to retail banking. In 1959 a standard for machine readable characters (MICR) was agreed and patented in the United States for use with cheques which led to the first automated reader/sorting machines. In the 1960 the first Automated Teller Machines (ATM) or Cash machines were developed and first machines started to appear by the end of the decade. Banks started to become heavy investors in computer technology to automate much of the manual processing, which saw the start of a shift by banks having a large number of clerical staff in favor of new automated systems. By the 1970s the first payment systems started to be develop that would lead to both Electronic payment systems for domestic and international payments. The international SWIFT network was established in 1973 and domestic payment systems were developed around the world by banks working together with governments.

1980s deregulation and globalisation

Bishopsgate in the City of London

Bishopsgate in the City of LondonGlobal banking and capital market services proliferated during the 1980s after deregulation of financial markets in a number of countries. The 1986 'Big Bang' in London allowing banks to access capital markets in new ways, which led to significant changes to the way banks operated and accessed capital. It also started a trend where retail banks started to acquire investment banks and stock brokers creating universal banks that offered a wide range of banking services. The trend also spread to the US after much of the Glass–Steagall Act was repealed in the 1980s, this saw US retail banks embark on big rounds of mergers and acquisitions and also engage in investment banking activities.

Financial services continued to grow through the 1980s and 1990s as a result of a great increase in demand from companies, governments, and financial institutions, but also because financial market conditions were buoyant and, on the whole, bullish. Interest rates in the United States declined from about 15% for two-year U.S. Treasury notes to about 5% during the 20-year period, and financial assets grew then at a rate approximately twice the rate of the world economy.

This period saw a significant internationalization of financial markets. The increase of U.S. Foreign investments from Japan not only provided the funds to corporations in the U.S., but also helped finance the federal government.

The dominance of U.S. financial markets[citation needed] was disappearing and there was an increasing interest in foreign stocks. The extraordinary growth of foreign financial markets results from both large increases in the pool of savings in foreign countries, such as Japan, and, especially, the deregulation of foreign financial markets, which enabled them to expand their activities. Thus, American corporations and banks started seeking investment opportunities abroad, prompting the development in the U.S. of mutual funds specializing in trading in foreign stock markets.

Such growing internationalization and opportunity in financial services changed the competitive landscape, as now many banks would demonstrated a preference for the “universal banking” model prevalent in Europe. Universal banks are free to engage in all forms of financial services, make investments in client companies, and function as much as possible as a “one-stop” supplier of both retail and wholesale financial services.

21st century

The consolidation was accomplished through acquisitions which grow in size over this period, and there were many of them. By the end of 2000, a year in which a record level of financial services transactions with a market value of $10.5 trillion occurred, the top ten banks commanded a market share of more than 80% and the top five, 55%. Of the top ten banks ranked by market share, seven were large universal-type banks (three American and four European), and the remaining three were large U.S. investment banks who between them accounted for a 33% market share.[citation needed]

This growth and opportunity also led to an unexpected outcome: entrance into the market of other financial intermediaries: non-bank financial institution. Large corporate players were beginning to find their way into the financial service community, offering competition to established banks. The main services offered included insurances, pension, mutual, money market and hedge funds, loans and credits and securities. Indeed, by the end of 2001 the market capitalisation of the world’s 15 largest financial services providers included four non-banks.

The process of financial innovation advanced enormously in the first decade of the 21 century increasing the importance and profitability of nonbank finance. Such profitability priorly restricted to the non-banking industry, has prompted the Office of the Comptroller of the Currency (OCC) to encourage banks to explore other financial instruments, diversifying banks' business as well as improving banking economic health. Hence, as the distinct financial instruments are being explored and adopted by both the banking and non-banking industries, the distinction between different financial institutions is gradually vanishing.

The first decade of the 21st century also saw the culmination of the technical innovation in banking over the previous 30 years and saw a major shift away from traditional banking to internet banking.

Late-2000s financial crisis

2007 bank run on Northern Rock, a UK bank

2007 bank run on Northern Rock, a UK bankThe Late-2000s financial crisis caused significant stress on banks around the world. The failure of a large number of major banks resulted in government bail-outs. The collapse and fire sale of Bear Stearns to JP Morgan Chase in March 2008 and the collapse of Lehman Brothers in September that same year led to a credit crunch and global banking crises. In response governments around the world bailed-out, nationalised or arranged fire sales for a large number of major banks. Starting with the Irish government on the 29 September 2008,[37] governments around the world even provide wholesale guarantees underwriting banks to avoid panic and systemic failure the whole banking system. These events spawned the term 'too big to fail' and resulted in a lot of discussion about moral hazard of these actions.

Major events in banking history

- Florentine banking - The Medicis and Pittis among others.

- 1100 - 1300 - Knights Templar run earliest Euro wide /Mideast banking.

- 1542 - 1551 - The Great Debasement refers to the English Crown’s policy of coement during the reigns of Henry VIII and Edward VI.

- 1602 – First joint-stock company, the Dutch East India Company founded.

- 1602 - The Amsterdam Stock Exchange was established by the Dutch East India Company for dealings in its printed stocks and bonds.

- 1609 - The Amsterdamsche Wisselbank (Amsterdam Exchange Bank) was founded.

- 1690s - The Massachusetts Bay Colony was the first of the Thirteen Colonies to issue permanently circulating banknotes.

- 1694 - The Bank of England was set up to supply money to the King.

- 1695 - The Parliament of Scotland creates the Bank of Scotland.

- 1716 - John Law opens Banque Générale

- 1717 - Master of the Royal Mint Sir Isaac Newton established a new mint ratio between silver and gold that had the effect of driving silver out of circulation (bimetalism)and putting Britain on a gold standard.

- 1720 – The South Sea Bubble and John Law's Mississippi Scheme, which caused a European financial crisis and forced many bankers out of business.

- 1775 – The first building society, Ketley's Building Society, was established in Birmingham, England.

- 1781 – The Bank of North America was found by the Continental Congress.

- 1791 - The First Bank of the United States was a bank chartered by the United States Congress. The charter was for 20 years.

- 1800 – Rothschild family founds Euro wide banking.

- 1816 - The Second Bank of the United States was chartered five years after the First Bank of the United States lost its charter. This charter was also for 20 years. The bank was created to finance the country in the aftermath of the War of 1812.

- 1862 - To finance the American Civil War, the federal government under U.S. President Abraham Lincoln issued a legal tender paper money, the "greenbacks".

- 1874 - The Specie Payment Resumption Act provided for the redemption of United States paper currency ("greenbacks"), in gold, beginning in 1879.

- 1913 - The Federal Reserve Act created the Federal Reserve System, the central banking system of the United States of America, and granted it the legal authority to issue legal tender.

- 1930–33 - In the wake of the Wall Street Crash of 1929, 9,000 banks close, wiping out a third of the money supply in the United States.[38]

- 1933 - Executive Order 6102 signed by U.S. President Franklin D. Roosevelt forbade ownership of Gold Coin, Gold Bullion, and Gold Certificates by U.S. citizens beyond a certain amount, effectively ending the convertibility of US dollars into gold.

- 1971 - The Nixon Shock was a series of economic measures taken by U.S. President Richard Nixon which canceled the direct convertibility of the United States dollar to gold by foreign nations. This essentially ended the existing Bretton Woods system of international financial exchange.

- 1986 – The "Big Bang" (deregulation of London financial markets) served as a catalyst to reaffirm London's position as a global centre of world banking.

- 2007 - Start of the Late-2000s financial crisis that saw the a credit crunch that led to the failure and bail-out of a large number of the worlds biggest banks.

- 2008 – Washington Mutual collapses. It was the largest bank failure in history.

See also

- History of money

- History of banking in China

- History of banking in the United States

- History of banking in Australia

- History of banking in India

- Online banking

- Subprime mortgage crisis

References

Footnotes

- ^ The word "bank" reflects the origins of banking in temples. According to the famous passage from the New Testament, when Christ drove the money changers out of the temple in Jerusalem, he overturned their tables. Matthew 21.12. In Greece, bankers were known as trapezitai, a name derived from the tables where they sat. Similarly, the English word bank comes from the Italian banca, for bench or counter.

Citations

- ^ a b Hoggson, N. F. (1926) Banking Through the Ages, New York, Dodd, Mead & Company.

- ^ Goldthwaite, R. A. (1995) Banks, Places and Entrepreneurs in Renaissance Florence, Aldershot, Hampshire, Great Britain, Variorum

- ^ "Evolution of Payment Systems in India =Reserve Bank of India". http://www.rbi.org.in/scripts/PublicationsView.aspx?id=155.

- ^ Wagel, Srinivas (1915). Chinese currency and banking. http://chestofbooks.com/finance/banking/Chinese-Currency-And-Banking/Chapter-VI-Banking-In-China.html.

- ^ Cohen, Edward: Athenian Economy and Society: A Banking Perspective (Princeton, NJ: Princeton University Press, 1992) ISBN 0-691-03609-8

- ^ Matyszak, Philip (2007). Ancient Rome on Five Denarii a Day. New York: Thames & Hudson. pp. 144. ISBN 050005147X. http://www.amazon.com/Ancient-Rome-Five-Denarii-Day/dp/050005147X.

- ^ Johnson cites Fritz E. Heichelcheim: An Ancient Economic History, 2 vols. (trans. Leiden 1965), i.104-566

- ^ Johnson, Paul: A History of the Jews (New York: HarperCollins Publishers, 1987) ISBN 0-06-091533-1. pp.172–173

- ^ The Hebrew Bible in English according to the JPS 1917 Edition. http://www.mechon-mamre.org/e/et/et0523.htm

- ^ The references cited in the Passionary for this woodcut: 1 John 2:14–16, Matthew 10:8, and The Apology of the Augsburg Confession, Article 8, Of the Church

- ^ Examples of debt:I Samuel 22:2, II Kings 4:1, Isaiah 50:1. Prophetic condemnation of usury: Ezekiel 22:12, Nehemiah 5:7 and 12:13. Cautions regarding debt: Prov 22:7, passim.

- ^ a b c d e Jewish Encyclopedia

- ^ Goldthwaite, R. A. (1995) Banks, Places and Entrepreneurs in Renaissance Florence, Aldershot, Hampshire, Great Britain, Variorum

- ^ Price Waterhouse Coopers Financial Year Book FYB, 2009)

- ^ İnalcik, Halil (1997). An economic and social history of the Ottoman Empire. Cambridge University Press. p. 213. http://books.google.com/books?id=1j-AtkBmn78C&pg=PA213&dq=Marrano+banking&hl=en&ei=0pDUTeuJG5TWtQOGjonMBw&sa=X&oi=book_result&ct=result&resnum=5&ved=0CE0Q6AEwBA#v=onepage&q=Marrano%20banking&f=false.

- ^ Dumper, Michael; Stanley, Bruce E. (2007). Cities of the Middle East and North Africa: a historical encyclopedia. ABC-CLIO. p. 185. http://books.google.com/books?id=3SapTk5iGDkC&pg=PA185&lpg=PA185&dq=Marrano+banking&source=bl&ots=8sTF94Oa1w&sig=S7EkbxOydN-srw4UCrlCHC1Ku8I&hl=en&ei=3-qeTb7gNqrdiAKG1omDAw&sa=X&oi=book_result&ct=result&resnum=5&ved=0CCkQ6AEwBA#v=onepage&q=Marrano%20banking&f=false.

- ^ İnalcık, Halil; Quataert, Donald (1994). An economic and social history of the Ottoman Empire, 1300-1914. Cambridge University Press. p. 212. http://books.google.com/books?id=MWUlNdskNfIC&pg=PA212&lpg=PA212&dq=Marrano+banking&source=bl&ots=b16xixwrg6&sig=6sSusKxzjnVmDGgqtDgo1ak5i7A&hl=en&ei=qemeTZTIMIrmiAKIu8yRAw&sa=X&oi=book_result&ct=result&resnum=3&ved=0CCIQ6AEwAg#v=onepage&q=Marrano%20banking&f=false.

- ^ Bosworth, Clifford Edmund (2007). Historic cities of the Islamic world. BRILL. p. 207. http://books.google.com/books?id=UB4uSVt3ulUC&pg=PA207&lpg=PA207&dq=Marrano+banking&source=bl&ots=FCF1tS1jvO&sig=cH30pGDMogt-dfeNPavF0VlHzww&hl=en&ei=3-qeTb7gNqrdiAKG1omDAw&sa=X&oi=book_result&ct=result&resnum=4&ved=0CCYQ6AEwAw#v=onepage&q=Marrano%20banking&f=false.

- ^ Black, Edwin (2004). Banking on Baghdad: inside Iraq's 7,000-year history of war, profit and conflict. John Wiley and Sons. p. 335. http://books.google.com/books?id=LVScQYzhx5oC&pg=PA335&dq=Jews+Banking&hl=en&ei=7CegTZWkKcfniALv8v3_Ag&sa=X&oi=book_result&ct=result&resnum=7&ved=0CEkQ6AEwBjiCAQ#v=onepage&q=Jews%20Banking&f=false. "Under Ottoman rule,during the eighteenth and nineteenth centuries, Jews continued to thrive, becoming part of the commercial and political ruling class. Like Armenians,the Jews could engage in necessary commercial activities, such as moneylending and banking, that were proscribed for Moslems under Islamic law."

- ^ a b c d e Dimont, Max (1962). "Jews, God, and History",. pp. 273–4. ISBN 978-0451529404.

- ^ a b Kreftz, Gerald (1984). Jews and Money: The Myths and the Reality. p. 46. ISBN 978-0899191294.

- ^ Perry, p 131

- ^ Sombart, Werner (1913). The Jews and Modern Capitalism. pp. 53–7. ISBN 978-0217352895.

- ^ "Guide to Checks and Check Fraud". Wachovia Bank. 2003. p. 4. https://www.wachovia.com/file/checks_and_check_fraud.pdf.

- ^ a b c "Banking Origin and Development". Invest and Income. http://www.investmentsandincome.com/banks-banking/banking_origin.html. Retrieved July 26, 2011.

- ^ Cameron, p 6-7

- ^ Perry, p 138

- ^ Cassis, p 66

- ^ Malamat, Abraham; Ben-Sasson, Haim Hillel (1976). A history of the Jewish people. Harvard University Press. p. 796.

- ^ Niall Ferguson, The House of Rothschild: Volume 2: The World's Banker: 1849-1999 (2000)

- ^ Richard Smethurst,"Takahasi Korekiyo, the Rothschilds and the Russo-Japanese War, 1904-1907". Retrieved 4 September 2007.

- ^ Larry Schweikart, "U.S. Commercial Banking: A Historiographical Survey," Business History Review, Autumn 1991, Vol. 65 Issue 3, pp 606-61

- ^ Joyce Appleby, The Relentless Revolution: A History of Capitalism (2010)

- ^ Fortune, Peter (Sept-Oct, 2000). "Margin Requirements, Margin Loans, and Margin Rates: Practice and Principles - analysis of history of margin credit regulations - Statistical Data Included". New England Economic Review. http://findarticles.com/p/articles/mi_m3937/is_2000_Sept-Oct/ai_80855422/pg_5.

- ^ a b "Bank Failures". Living History Farm. http://www.livinghistoryfarm.org/farminginthe30s/money_08.html. Retrieved 2008-05-22.

- ^ "Friedman and Schwartz, Monetary History of the United States", 352

- ^ "Bank Guarantee Scheme & Recapitalisation". National Treasury Management Agency. October 22, 2008. http://www.ntma.ie/IrishEconomy/bankGuaranteeScheme.php.

- ^ Hawkins, William, "Panic Control", The Washington Times, 12 May 2008

Further reading

- Cameron, Rondo. Banking in the Early Stages of Industrialization: A Study in Comparative Economic History (1967)

- Cameron, Rondo et al. International Banking 1870–1914 (1992) excerpt and text search

- Grossman, Richard S. Unsettled Account: The Evolution of Banking in the Industrialized World Since 1800 (Princeton University Press; 2010) 384 pages. Considers how crises, bailouts, mergers, and regulations have shaped the history of banking in Western Europe, the United States, Canada, Japan, and Australia.

- Hammond, Bray, Banks and Politics in America, from the Revolution to the Civil War, Princeton : Princeton University Press, 1957.

- Rothbard, Murray N., History of Money and Banking in the United States. Full text (510 pages) in pdf format

- For French banking history, read the History of banks in France (in English or in French) on the FBF website.

- Giuseppe Felloni and Guido Laura, Genoa and the history of finance: A series of firsts? 9 November 2004, ISBN 88-87822-16-6

Categories:

Wikimedia Foundation. 2010.