- Mortgage law

-

This article is about the legal mechanisms used to secure the performance of obligations, including the payment of debts, with property. For loans secured by mortgages, such as residential housing loans, and lending practices or requirements, see Mortgage loan.

A mortgage is a security interest in real property held by a lender as a security for a debt, usually a loan of money. A mortgage in itself is not a debt, it is the lender's security for a debt. It is a transfer of an interest in land (or the equivalent) from the owner to the mortgage lender, on the condition that this interest will be returned to the owner when the terms of the mortgage have been satisfied or performed. In other words, the mortgage is a security for the loan that the lender makes to the borrower.

The word is a Law French term meaning "dead pledge," apparently meaning that the pledge ends (dies) either when the obligation is fulfilled or the property is taken through foreclosure.[1]

In most jurisdictions mortgages are strongly associated with loans secured on real estate rather than on other property (such as ships) and in some jurisdictions only land may be mortgaged. A mortgage is the standard method by which individuals and businesses can purchase real estate without the need to pay the full value immediately from their own resources. See mortgage loan for residential mortgage lending, and commercial mortgage for lending against commercial property.

Contents

Participants and variant terminology

Legal systems in different countries, while having some concepts in common, employ different terminology. However, in general, a mortgage of property involves the following parties. The borrower, known as the mortgagor, gives the mortgage to the lender, known as the mortgagee.

Lender/mortgagee

A mortgage lender is an investor that lends money secured by a mortgage on real estate. In today's world, most lenders sell the loans they write on the secondary mortgage market. When they sell the mortgage, they earn revenue called Service Release Premium. Typically, the purpose of the loan is for the borrower to purchase that same real estate. As the mortgagee, the lender has the right to sell the property to pay off the loan if the borrower fails to pay.

The mortgage runs with the land, so even if the borrower transfers the property to someone else, the mortgagee still has the right to sell it if the borrower fails to pay off the loan.

So that a buyer cannot unwittingly buy property subject to a mortgage, mortgages are registered or recorded against the title with a government office, as a public record. The borrower has the right to have the mortgage discharged from the title once the debt is paid.

Borrower/mortgagor

A mortgagor is the borrower in a mortgage—he owes the obligation secured by the mortgage. Generally, the debtor must meet the conditions of the underlying loan or other obligation and the conditions of the mortgage. Otherwise, the debtor usually runs the risk of foreclosure of the mortgage by the creditor to recover the debt. Typically the debtors will be the individual homeowners, landlords, or businesses who are purchasing their property by way of a loan.

Other participants

Because of the complicated legal exchange, or conveyance, of the property, one or both of the main participants are likely to require legal representation. The terminology varies with legal jurisdiction; see lawyer, solicitor and conveyancer.

Because of the complex nature of many markets the debtor may approach a mortgage broker or financial adviser to help him or her source an appropriate creditor, typically by finding the most competitive loan.

The debt is, in civil law jurisdictions, referred to as hypothecation, which may make use of the services of a hypothecary to assist in the hypothecation.

History

The practice of securing land for payment of money in English law dates back to Anglo-Saxon England.[2] The practice has been named variously as vadium mortuum by Thomas de Littleton and mortuum vadium by William Blackstone, and translated as dead pledge in English and mortgage in French.[3] At common law, a mortgage was a conveyance of land that on its face was absolute and conveyed a fee simple estate, but which was in fact conditional, and would be of no effect if certain conditions were met – usually, but not necessarily, the repayment of a debt to the original landowner in the form of promissory note.

The debt was absolute in form, and unlike a "live pledge" was not conditionally dependent on its repayment solely from raising and selling crops or livestock or simply giving the crops and livestock raised on the mortgaged land. The mortgage debt remained in effect whether or not the land could successfully produce enough income to repay the debt. In theory, a mortgage required no further steps to be taken by the creditor, such as acceptance of crops and livestock in repayment. The difficulty with this arrangement was that the lender was absolute owner of the property and could sell it or refuse to reconvey it to the borrower, who was in a weak position. Increasingly the courts of equity began to protect the borrower's interests, so that a borrower came to have an absolute right to insist on reconveyance on redemption. This right of the borrower is known as the "equity of redemption".

This arrangement, whereby the lender was in theory the absolute owner, but in practice had few of the practical rights of ownership, was seen in many jurisdictions as being awkwardly artificial. By statute the common law's position was altered so that the mortgagor would retain ownership, but the mortgagee's rights, such as foreclosure, the power of sale, and the right to take possession, would be protected. In the United States, those states that have reformed the nature of mortgages in this way are known as lien states. A similar effect was achieved in England and Wales by the Law of Property Act 1925, which abolished mortgages by the conveyance of a fee simple.

Since the seventeenth century, lenders have not been allowed to carry interest in the property beyond the underlying debt under the equity of redemption principle. Attempts by the lender to carry an equity interest in the property in a manner similar to convertible bonds through contract have been therefore struck down by courts as "clogs", but developments in the 1980s and 1990s have led to less rigid enforcement of this principle, particularly due to interest among theorists in returning to a freedom of contract regime.[4]

Default on divided property

When a tract of land is purchased with a mortgage and then split up and sold, the "inverse order of alienation rule" applies to decide parties liable for the unpaid debt.

When a mortgaged tract of land is split up and sold, upon default, the mortgagee first forecloses on lands still owned by the mortgagor and proceeds against other owners in an 'inverse order' in which they were sold. For example, A acquires a 3-acre (12,000 m2) lot by mortgage then splits up the lot into three 1-acre (4,000 m2) lots (A, B, and C), and sells lot B to X, and then lot C to Y, retaining lot A for himself. Upon default, the mortgagee proceeds against lot A first, the mortgagor. If foreclosure or repossession of lot A does not fully satisfy the debt, the mortgagee proceeds against lot B, then lot C. The rationale is that the first purchaser should have more equity and subsequent purchasers receive a diluted share.

Legal aspects

Mortgages may be legal or equitable. Furthermore, a mortgage may take one of a number of different legal structures, the availability of which will depend on the jurisdiction under which the mortgage is made. Common law jurisdictions have evolved two main forms of mortgage: the mortgage by demise and the mortgage by legal charge.

Mortgage by demise

In a mortgage by demise, the mortgagee (the lender) becomes the owner of the mortgaged property until the loan is repaid or other mortgage obligation fulfilled in full, a process known as "redemption". This kind of mortgage takes the form of a conveyance of the property to the creditor, with a condition that the property will be returned on redemption.

Mortgages by demise were the original form of mortgage, and continue to be used in many jurisdictions, and in a small minority of states in the United States. Many other common law jurisdictions have either abolished or minimised the use of the mortgage by demise. For example, in England and Wales this type of mortgage is no longer available in relation to registered interests in land, by virtue of section 23 of the Land Registration Act 2002 (though it continues to be available for unregistered interests).

Mortgage by legal charge

In a mortgage by legal charge or technically "a charge by deed expressed to be by way of legal mortgage",[5] the debtor remains the legal owner of the property, but the creditor gains sufficient rights over it to enable them to enforce their security, such as a right to take possession of the property or sell it.

To protect the lender, a mortgage by legal charge is usually recorded in a public register. Since mortgage debt is often the largest debt owed by the debtor, banks and other mortgage lenders run title searches of the real estate property to make certain that there are no mortgages already registered on the debtor's property which might have higher priority. Tax liens, in some cases, will come ahead of mortgages. For this reason, if a borrower has delinquent property taxes, the bank will often pay them to prevent the lienholder from foreclosing and wiping out the mortgage.

This type of mortgage is most common in the United States and, since the Law of Property Act 1925,[5] it has been the usual form of mortgage in England and Wales (it is now the only form for registered interests in land – see above).

In Scotland, the mortgage by legal charge is also known as Standard Security.[6]

In Pakistan, the mortgage by legal charge is most common way used by banks to secure the financing.[citation needed] It is also known as registered mortgage. After registration of legal charge, the bank's lien is recorded in the land register stating that the property is under mortgage and cannot be sold without obtaining an NOC (No Objection Certificate) from the bank.

Equitable mortgage

See also: Security interest#Types of securityEquitable mortgages don't fit the criteria for a legal mortgage, but are considered mortgages under equity (in the interests of justice) because money was lent and security was promised. This could arise because of procedural or paperwork issues. Based on this definition, there are numerous situations which could lead to an equitable mortgage.[7] As of 1961, English law required the consent of the court before the equitable mortgagee was allowed to sell.[8] When the borrower deposits a title deed with the lender, it has historically created an equitable mortgage in England, but the creation of an equitable mortgage by such a process has been less certain in the United States.[9]

In an equitable mortgage the lender is secured by taking possession of all the original title documents of the property and by borrower's signing a Memorandum of Deposit of Title Deed (MODTD). This document is an undertaking by the borrower that he/she has deposited the title documents with the bank with his own wish and will, in order to secure the financing obtained from the bank..

Foreclosure and non-recourse lending

See also: Strategic defaultIn most jurisdictions, a lender may foreclose on the mortgaged property if certain conditions – principally, non-payment of the mortgage loan – apply. Subject to local legal requirements, the property may then be sold. Any amounts received from the sale (net of costs) are applied to the original debt.

In some jurisdictions mainly in the United States,[10] mortgage loans are non-recourse loans: if the funds recouped from sale of the mortgaged property are insufficient to cover the outstanding debt, the lender may not have recourse to the borrower after foreclosure. In other jurisdictions, the borrower remains responsible for any remaining debt, through a deficiency judgment. In some jurisdictions, first mortgages are non-recourse loans, but second and subsequent ones are recourse loans.

Specific procedures for foreclosure and sale of the mortgaged property almost always apply, and may be tightly regulated by the relevant government. In some jurisdictions, foreclosure and sale can occur quite rapidly, while in others, foreclosure may take many months or even years. In many countries, the ability of lenders to foreclose is extremely limited, and mortgage market development has been notably slower.

Mortgages in the United States

Types of mortgage instruments

Two types of mortgage instruments are commonly used in the United States: the mortgage (sometimes called a mortgage deed) and the deed of trust.[11]

The mortgage

In all but a few states, a mortgage creates a lien on the title to the mortgaged property. Foreclosure of that lien almost always requires a judicial proceeding declaring the debt to be due and in default and ordering a sale of the property to pay the debt.[citation needed] Many "mortgages" contain a power of sale clause, also known as nonjudicial foreclosure clause, making them tantamount to a deed of trust. Most "mortgages" in California are actually deeds of trust.[12] The effective difference is that the foreclosure process can be much faster for a deed of trust than for a mortgage, on the order of 3 months rather than a year. Because the foreclosure does not require actions by the court the transaction costs can be quite a bit less.[citation needed]

The deed of trust

Main article: trust deed (real estate)The deed of trust is a deed by the borrower to a trustee for the purposes of securing a debt. In most states, it also merely creates a lien on the title and not a title transfer, regardless of its terms. It differs from a mortgage in that, in many states, it can be foreclosed by a non-judicial sale held by the trustee through a "power of sale".[13] It is also possible to foreclose them through a judicial proceeding.[citation needed]

Deeds of trust to secure repayments of debts should not be confused with trust instruments that are sometimes called deeds of trust but that are used to create trusts for other purposes, such as estate planning. Though there are superficial similarities in the form, many states hold deeds of trust to secure repayment of debts do not create true trust arrangements.[citation needed]

Security deed

The deed to secure debt is a mortgage instrument used in the state of Georgia. Unlike a mortgage, a security deed is an actual conveyance of real property in security of a debt. Upon the execution of such a deed, title passes to the grantee or beneficiary (usually lender), however the grantor (debtor) maintains equitable title to use and enjoy the conveyed land subject to compliance with debt obligations.

Security deeds must be recorded in the county where the land is located. Although there is no specific time within which such deeds must be filed, the failure to timely record the deed to secure debt may affect priority and therefore the ability to enforce the debt against the subject property.[14]

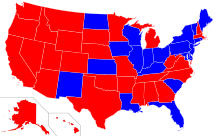

"Title theory" and "lien theory"

Map showing title theory (red) and lien theory (blue) states

Map showing title theory (red) and lien theory (blue) states

In the United States, some states are "title theory" states while most are "lien theory" state.[15] In lien theory states, a mortgage or a deed of trust will create a mortgage lien upon the title to the real property being mortgaged, while the mortgagor still holds both legal and equitable title. In title theory states, a mortgage is a transfer of legal title to secure a debt, while the mortgagor still retains equitable title.[16]

Priority

The lien is said to "attach" to the title when the mortgage is signed by the mortgagor and delivered to the mortgagee and the mortgagor receives the funds whose repayment the mortgage secures. Subject to the requirements of the recording laws of the state in which the land is located, this attachment establishes the priority of the mortgage lien with respect to most other liens[17] on the property's title.[18] Liens that have attached to the title before the mortgage lien are said to be senior to, or prior to, the mortgage lien. Those attaching afterward are said to be junior or subordinate.[19] The purpose of this priority is to establish the order in which lien holders are entitled to foreclose their liens in an attempt to recover their debts. If there are multiple mortgage liens on the title to a property and the loan secured by a first mortgage is paid off, the second mortgage lien will move up in priority and become the new first mortgage lien on the title. Documenting this new priority arrangement will require the release of the mortgage securing the paid off loan.

Assignment

Mortgages, along with the Mortgage note, may be assigned to other parties. Some jurisdictions hold that the assignment of the note implies the assignment of the mortgage, while others contend it only creates an equitable right.

See also

- Hypothec

- Loan servicing

- Trust deed

- Bridge financing

- Financing

- Fixed rate mortgage

- Promissory note

- Loan origination

- Subprime lending

- Mortgage calculator

- Refinancing

- Foreign currency mortgage

- Americans for Fairness in Lending

- National Mortgage News

- Mortgage insurance

- Collateralized mortgage obligation - CMO

- Subprime mortgage crisis

Notes and references

- ^ Coke, Edward. Commentaries on the Laws of England. "[I]f he doth not pay, then the Land which is put in pledge upon condition for the payment of the money, is taken from him for ever, and so dead to him upon condition, &c. And if he doth pay the money, then the pledge is dead as to the Tenant"

- ^ Jones, Leonard Augustus (1904). A treatise on the law of mortgages of real property, Volume 1.. Link at Google Books

- ^ Tomlins, Thomas Edlyne (1811). The Law-dictionary: Explaining the Rise, Progress, and Present State, of the English Law; Defining and Interpreting the Terms Or Words of Art; and Comprising Copious Information on the Subjects of Law, Trade, and Government, Volume 4.. Link at Google Books

- ^ Shanker M. (2003). Will Mortgage Law Survive? Case Western Reserve Law Review 54:1.

- ^ a b "Law of Property Act 1925 (c.20) Part III Mortgages, Rentcharges, and Powers of Attorney". Ministry of Justice. http://www.statutelaw.gov.uk/content.aspx?LegType=All+Primary&PageNumber=84&NavFrom=2&parentActiveTextDocId=432552&activetextdocid=432650. Retrieved 2008-01-30.

- ^ "Nemo Loans Jargon Buster". Nemo Personal Finance Ltd. http://www.nemo-loans.co.uk/qna/nemo-loans-jargon-buster.php. Retrieved 2009-02-10.

- ^ Davis G. (1956). The Equitable Mortgage in Kansas. Kansas Law Review.

- ^ Hannigan ASJ. The Imposition of Western Law Forms upon Primitive Societies. Comparative Studies in Society and History.

- ^ Cocke WA. Equitable Mortgage by Deposit of Title Deeds-The American and English Rule. The Central Law Journal.

- ^ Ghent, Andra C. and Kudlyak, Marianna, Recourse and Residential Mortgage Default: Theory and Evidence from U.S. States (July 10, 2009). Federal Reserve Bank of Richmond Working Paper No. 09-10. Available at SSRN: http://ssrn.com/abstract=1432437. The authors classify 11 states as nonrecourse.

- ^ Kratovil, Robert; Werner, R. (1988). Real Estate Law (9th ed.). Prentice-Hall, Inc.. Sec 20.09. ISBN 0-13-763343-2.

- ^ See the discussion of background principles of California real property law in Alliance Mortgage Co. v. Rothwell, 10 Cal. 4th 1226, 1235-1238 (1995).

- ^ Kratovil, Robert; Werner, R. (1988). Real Estate Law (9th ed.). Prentice-Hall, Inc.. Sec 20.09(b). ISBN 0-13-763343-2.

- ^ Security Interests in Georgia, By Steven M. Mills of Steven M. Mills, P.C.[1] (1999).

- ^ Kratovil, Robert; Werner, R. (1981). Modern Mortgage Law and Practice (2nd ed.). Prentice-Hall, Inc.. Sec 1.6. ISBN 9780135957448.

- ^ U.S. Bank v. Ibanez, Massachusetts Supreme Judicial Court, SJC-10694, January 7, 2011, page 12. See Bank Stocks Slump On Foreclosure Ruling, New York Times Dealbook.

- ^ Exceptions include real estate tax liens and, in most states, mechanic's liens.

- ^ The failure to record a previously made mortgage may, under some circumstances, allow a subsequent mortgagee's mortgage to be recognized as prior in right to the otherwise prior mortgage.

- ^ Of course, the lienholders can agree among themselves to a different priority arrangement through subordination arrangements. See, R. Kratovil and R. Werner Modern Mortgage Law and Practice Chs. 30 & 38 (2nd Ed. Prentice-Hall, Inc.)

Categories:

Wikimedia Foundation. 2010.